- 2020ー2024年

- 2026-2035年

- 必要に応じて日本語レポートが入手可能

品質と信頼の証

持続可能な航空燃料市場規模

2026―2035年の持続可能な航空燃料市場の規模はどのくらいですか?

持続可能な航空燃料(SAF)市場に関する当社の調査レポートによると、同市場は予測期間(2026―2035年)の間に複利年間成長率(CAGR)約42.5%で成長すると予想されています。2035年には、世界市場規模は約784億米ドルに達すると見込まれています。しかし、当社の調査アナリストによると、基準年である2025年の市場規模は約21億米ドルと記録されています。

持続可能な航空燃料市場において、市場シェアの面でどの地域が優位を占めると予想されますか?

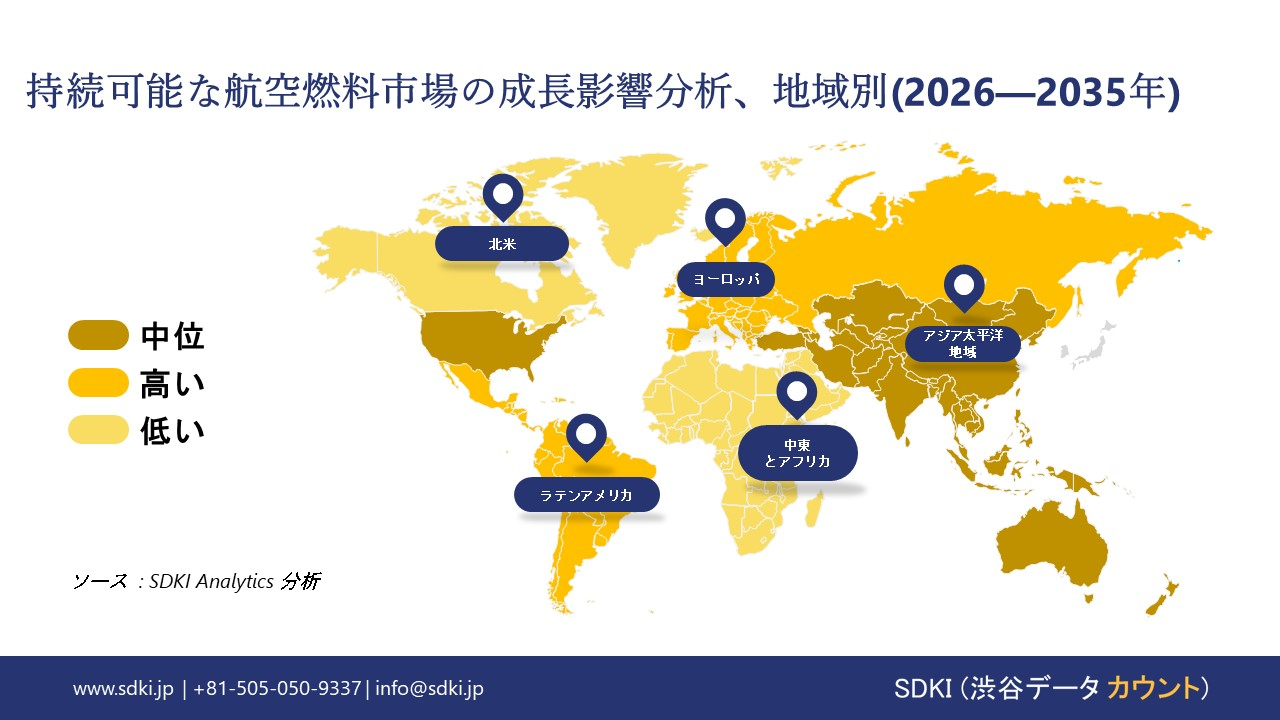

持続可能な航空燃料に関する当社の市場調査によると、北米は確立されたバイオ燃料義務化政策と主要航空会社との燃料購入契約に支えられ、市場シェアの約52%を占め、圧倒的なシェアを誇っています。一方、アジア太平洋地域は最も高い複利年間成長率(CAGR)で成長すると予想され、将来的に大きなビジネスチャンスが見込まれます。この成長加速は主に、同地域の野心的な国家脱炭素化ロードマップ、ネットゼロ目標への航空会社の取り組みの強化、そして生産能力拡大のためのバイオ精製インフラへの戦略的投資によって支えられています。

持続可能な航空燃料市場分析

持続可能な航空燃料とは何ですか?

持続可能な航空燃料(SAF)市場は、廃油、農業残渣、バイオマスなどの持続可能な原料から作られる、クリーン燃焼型のバイオベースジェット燃料代替品で構成されています。この燃料は、従来のジェット燃料と比較してライフサイクル全体での炭素排出量を大幅に削減し、航空業界の脱炭素化と気候変動対策目標を支援します。

持続可能な航空燃料市場における最近の傾向は何ですか?

当社の持続可能な航空燃料市場分析調査レポートによると、以下の市場傾向と要因が市場成長の主要な推進力として貢献すると予測されています。

- 航空脱炭素化義務化の拘束力により、持続可能-

な航空燃料(SAF)の需要が保証される – 当社の調査レポートによると、航空会社にライフサイクル温室効果ガス排出量の削減を義務付ける規制により、世界的に持続可能な航空燃料に対する非裁量的な需要が生まれています。ヨーロッパ連合(EU)では、ReFuelEU航空規制が2025年1月に発効し、EUの空港で供給される航空燃料には2025年までに2%のSAFを含まなければならないと義務付け、2030年までに6%、2050年までに70%に引き上げられる予定です。この規制はEU加盟国全体に一律に適用され、供給業者と航空会社の不確実性を排除します。同様に、米国では、連邦政府機関が調達とサプライチェーンを調整するとともに、2030年までに30億ガロン、2050年までに350億ガロンのSAF生産を目指すSAFグランドチャレンジの下でSAFの展開を実施しています。こうした拘束力のある義務付けは、燃料供給業者と航空会社に対し、価格変動に関わらずSAF(持続可能な航空燃料)の供給量を確保することを法的に義務付けるものであり、気候変動対策政策を主要な需要促進要因へと転換させるものであります。

- 航空会社の長期オフテイク契約によりSAFが融資可能なインフラ資産に転換 –

当社の調査レポートによると、航空会社は長期SAFオフテイク契約を締結しており、これによりSAF生産は投機的な供給からインフラのような資産へと転換しています。ユナイテッド航空は、2025年に提出した2024年版フォーム10-Kで、脱炭素化戦略の一環として、SAF生産者への大規模な株式投資とともに、一貫したSAF購入契約について言及しました。同様に、エールフランス-KLMは、 2024年版統合登録文書で、SAF調達がEUの規制要件と企業の気候目標を満たす上で中心的な役割を果たすことを確認しました。これらの契約により、SAF生産者は複数年にわたる収益の見通しを得ることができ、それによって債務による資金調達と規模拡大が可能になります。

持続可能な航空燃料市場は、日本の市場参加者にどのようなメリットをもたらすのか?

持続可能な航空燃料市場は、政府の政策や新たな生産イニシアチブに基づき、国内及び輸出バリューチェーン全体にわたって日本の市場プレーヤーに数多くの機会を提供しています。日本のGX基本政策の下、政府は予測期間中に国内航空燃料使用量の10%をSAFで代替するという目標を公式に設定しました。これは、航空の脱炭素化に向けた供給拡大と技術開発をさらに促進します。エネルギー供給構造強化法に基づくその他の措置には、技術開発に対する大幅な支援や、国内SAF生産に関連する税額控除などの投資インセンティブが含まれます。さらに、日本はSAFサプライチェーン開発を調整するために、経済産業省と国土交通省が共同でSAF官民協議会を設立しました。これに加え、コスモエナジーホールディングスは、経済産業省の2024年度SAF生産補助金を獲得し、三井物産などのパートナー企業とともに、バイオエタノールからジェット燃料への転換を商業化し、国内のSAF供給インフラを構築しています。コスモは既に国際的な持続可能性認証を取得した国産SAFを量産しており、2025年には航空会社や物流顧客への供給を拡大する予定です。これらの政策と企業の取り組みは、政策目標と事業運営を整合させ、国内外のSAFバリューチェーンにおける生産者、技術ライセンサー、物流サービス企業、そして下流の導入企業に収益機会を創出します。

持続可能な航空燃料市場に影響を与える主な制約要因は何ですか?

持続可能な航空燃料市場における主な制約要因は、高価な原料と未発達で複雑な変換技術のため、従来のジェット燃料に比べて製造コストが著しく高いことであります。この価格差が、抜本的な規制や補助金なしには、SAFの普及を阻んでいます。

サンプル納品物ショーケース

- 調査競合他社と業界リーダー

- 過去のデータに基づく予測

- 会社の収益シェアモデル

- 地域市場分析

- 市場傾向分析

持続可能な航空燃料市場レポートの洞察

持続可能な航空燃料市場の将来展望はどうなっていますか?

持続可能な航空燃料市場の世界シェアに関するレポートの洞察は以下のとおりです。

|

レポートのインサイト |

|

|

2026―2035年の複利年間成長率(CAGR) |

42.5% |

|

2025年の市場価値 |

21億米ドル |

|

2035年の市場価値 |

784億米ドル |

|

過去のデータ共有 |

過去5年間から2024年まで |

|

未来予測完了 |

2035年までの今後10年間 |

|

ページ数 |

200+ページ |

ソース: SDKI Analytics 専門家分析

持続可能な航空燃料市場はどのように分割されていますか?

当社は、持続可能な航空燃料市場の見通しに関連する様々な分野における需要と機会を説明する調査を実施しました。市場は、原料タイプ別、生産経路別、エンドユーザー別、分布別にセグメントに分割されていています。

持続可能な航空燃料市場は、原料タイプ別どのように分割されていますか?

原料タイプ別に基づいて、持続可能な航空燃料市場は、使用済み食用油/廃油、農業残渣/セルロース、エネルギー作物(例:キャメリーナ)、藻類/先端原料に分割されています。調査レポートによると、使用済み食用油/廃油は、 SAF生産のための費用対効果が高く拡張性のある原料として広く採用されていることを反映して‑、 2035年までに市場の34%を占めると予想されています。こうした廃棄物由来の原料は、本来であれば廃棄されるはずの資源を低炭素な航空燃料へと転換する助けとなり、サーキュラーエコノミー(循環型経済)としての価値を生み出しています。国際航空運送協会(IATA)によると、SAF(持続可能な航空燃料)の生産量は2024年に約1百万トン(13億リットル)に達し、2023年の0.5百万トンから倍増しました。もっとも、これは依然として世界のジェット燃料使用量の約0.3%に過ぎません。この着実な生産拡大は、SAF分野の急速な成長を示す一方で、現在の生産量と将来の需要との間に依然として大きな隔たりがあることも浮き彫りにしています。使用済み食用油やそれに類する廃棄物由来の原料は、今後もHEFA(水素化処理エステル・脂肪酸)製造プロセスの主要原料としての役割を果たし続け、SAFの初期導入を支えるとともに、各地で導入されているバイオ燃料の利用義務化政策の達成にも貢献していくと見込まれます。航空部門の脱炭素化に向け、低炭素ソリューションを重視する政策や航空会社による自主的な取り組みがますます加速していることから、こうした原料に対する市場の見通しは引き続き強気なものとなっています。

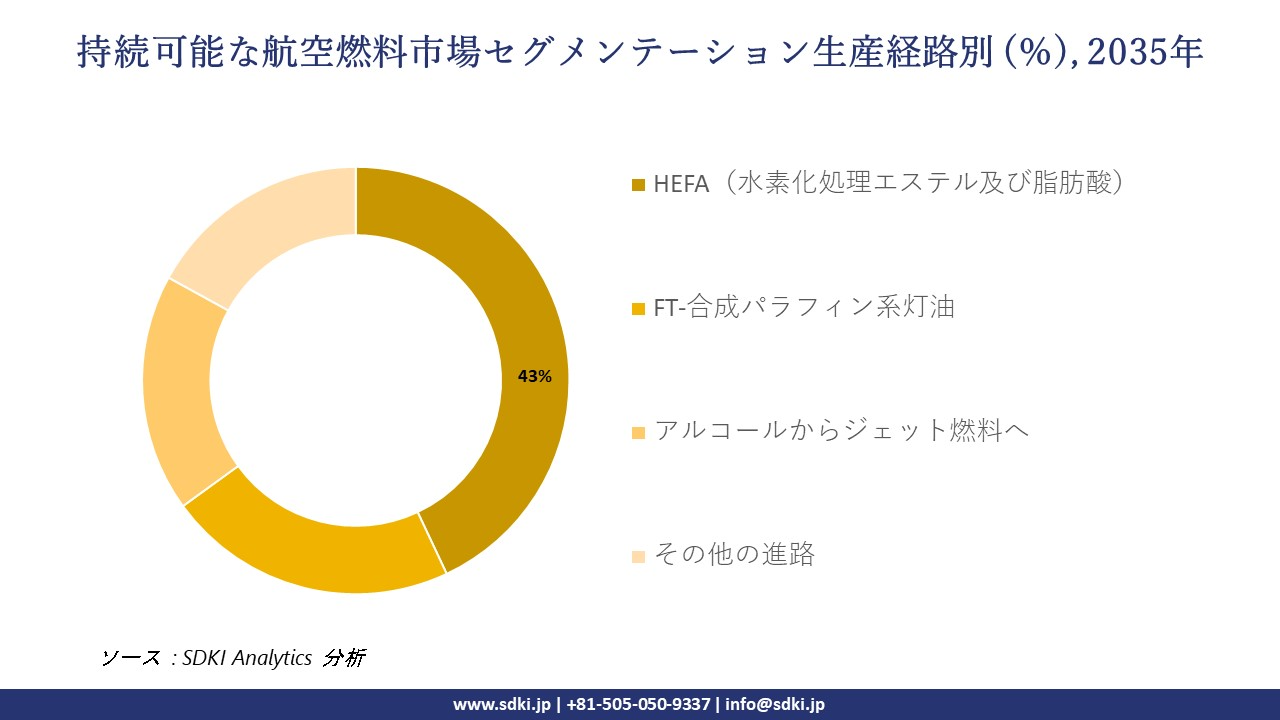

持続可能な航空燃料市場は、生産経路別にどのように分割されていますか?

持続可能な航空燃料市場は、生産経路別に基づいて、HEFA(水素化処理エステル及び脂肪酸)、FT-合成パラフィン系灯油、アルコールからジェット燃料へ、その他の進路に分割されています。調査レポートによると、 HEFA(水素化処理エステル及び脂肪酸)、広く採用されているSAF製造技術であるため、2035年までに43%の最大のシェアを占めると予測されています。HEFAプロセスは、脂肪、油、グリースを‑航空機の改造なしに既存の燃料規格を満たすドロップインジェット燃料に変換します。この製造経路は、従来のジェット燃料と比較してライフサイクル温室効果ガス排出量を削減する再生可能な代替燃料への需要が高まるにつれて、引き続き市場をリードしていきます。

持続可能な航空燃料市場に適用されるセグメントの一覧を以下に示します。

|

親セグメント |

サブセグメント |

|

原料タイプ別

|

|

|

生産経路別

|

|

|

エンドユーザー別

|

|

|

分布別

|

|

ソース: SDKI Analytics 専門家分析

持続可能な航空燃料市場の傾向分析と将来予測:地域別市場概況

アジア太平洋地域は、フライト数の増加と持続可能な燃料使用に関する政府主導の国家的な混合義務化により、持続可能な航空燃料の発展途上市場となっています。これらの要因が相まって、予測期間中に市場は複利年間成長率(CAGR)42.9%という最速の成長を遂げています。日本では、日本航空が2030年までに機内燃料の10%を代替するという目標を設定しており、同地域を代表する航空会社です。同様に、インド民間航空省は「グリーン航空」イニシアチブの下、2027年までに1%、2028年までに2%、2030年までに5%のSAF混合率という目標を設定しています。これにより、同地域におけるSAFの使用率は時間とともに増加し、強力な市場が形成されています。

SDKI Analyticsの専門家は、持続可能な航空燃料市場に関するこの調査レポートのために、以下の国と地域を調査しました。

|

地域 |

国 |

|

北米 |

|

|

ヨーロッパ |

|

|

アジア太平洋地域 |

|

|

ラテンアメリカ |

|

|

中東及びアフリカ |

|

ソース: SDKI Analytics 専門家分析

北米における持続可能な航空燃料市場の実績はどのようなものですか?

米国政府のSAFグランドチャレンジと混合義務化は、北米地域におけるSAF利用の強力な推進力となっています。エネルギー省、運輸省、農務省は、SAFグランドチャレンジの下、2030年までに年間30億ガロン、2050年までに350億ガロンのSAFを生産するという政府全体の目標を設定しています。これは、環境保護庁(EPA)が再生可能燃料基準(RFS)の下で提案している混合義務化によって補完されています。これらの支援的な義務化により、北米市場は52%のシェアを獲得し、世界をリードすると期待されている。EPAは、2024年と2025年について、SAFを含むバイオマス由来ディーゼルと先進バイオ燃料のカテゴリーごとに具体的な生産量目標を提案しています。野心的な生産目標と規制遵守メカニズムを組み合わせた規制の確実性は、燃料生産者と航空会社にとって明確な需要シグナルとなります。

持続可能な航空燃料調査の場所

北米(米国およびカナダ)、ラテンアメリカ(ブラジル、メキシコ、アルゼンチン、その他のラテンアメリカ)、ヨーロッパ(英国、ドイツ、フランス、イタリア、スペイン、ハンガリー、ベルギー、オランダおよびルクセンブルグ、NORDIC(フィンランド、スウェーデン、ノルウェー) 、デンマーク)、アイルランド、スイス、オーストリア、ポーランド、トルコ、ロシア、その他のヨーロッパ)、ポーランド、トルコ、ロシア、その他のヨーロッパ)、アジア太平洋(中国、インド、日本、韓国、シンガポール、インドネシア、マレーシア) 、オーストラリア、ニュージーランド、その他のアジア太平洋地域)、中東およびアフリカ(イスラエル、GCC(サウジアラビア、UAE、バーレーン、クウェート、カタール、オマーン)、北アフリカ、南アフリカ、その他の中東およびアフリカ

競争力ランドスケープ

SDKI Analyticsの調査員によると、持続可能な航空燃料市場の見通しは、大企業と中小企業といった規模の異なる企業間の市場競争により、分割されています。調査報告書によると、市場参加者は、製品や技術の発表、戦略的提携、協力、買収、事業拡大など、あらゆる機会を活用して、市場全体の見通しにおいて競争優位性を獲得しようとしています。

持続可能な航空燃料市場で事業を展開する主要なグローバル企業はどこですか?

当社の調査報告書によると、世界の持続可能な航空燃料市場の成長において重要な役割を担う主要企業には、 Neste Oyj、World Energy、Gevo, Inc.、Fulcrum BioEnergy, Inc.、SkyNRGなどが含まれます。

持続可能な航空燃料市場で競合する主要な日本企業はどこですか?

市場見通しによると、日本の持続可能な航空燃料市場の上位5社は、Mitsubishi Corporation, IHI Corporation, JERA Co. Inc., Cosmo Oil Company Ltd., ENEOS Corporationなどであります。

この市場調査レポートには、世界の持続可能な航空燃料市場分析調査レポートにおける主要企業の詳細な競合分析、企業プロファイル、最近の傾向、及び主要な市場戦略が含まれています。

持続可能な航空燃料市場における最新のニュースや傾向は何ですか?

- 行進 2025年:Airbusは、燃料が他の場所で使用された場合でも購入者がSAFの排出削減を申請できるようにすることで、供給と需要を促進する新たな「予約・申請」SAFイニシアチブを発表しました。このパイロットプログラムは、小規模事業者がSAFを入手しやすくし、認証登録制度を通じて持続可能性に関する特性を標準化することで、世界的なSAF市場の普及を加速させます。

- 2月 2025年:Euglena Co. Ltdは日本の SAF導入推進官民‑協議会は、政府及び業界と連携してSAFの普及を加速させるべく活動しています。経済産業省と国土交通省の支援を受け、同協議会は日本の航空業界におけるSAF利用拡大に向けた技術的・経済的な課題に取り組んでいます。

持続可能な航空燃料主な主要プレーヤー

主要な市場プレーヤーの分析

日本市場のトップ 5 プレーヤー

目次

持続可能な航空燃料マーケットレポート

関連レポート

よくある質問

- 2020ー2024年

- 2026-2035年

- 必要に応じて日本語レポートが入手可能

品質と信頼の証