- 2020ー2024年

- 2026-2035年

- 必要に応じて日本語レポートが入手可能

品質と信頼の証

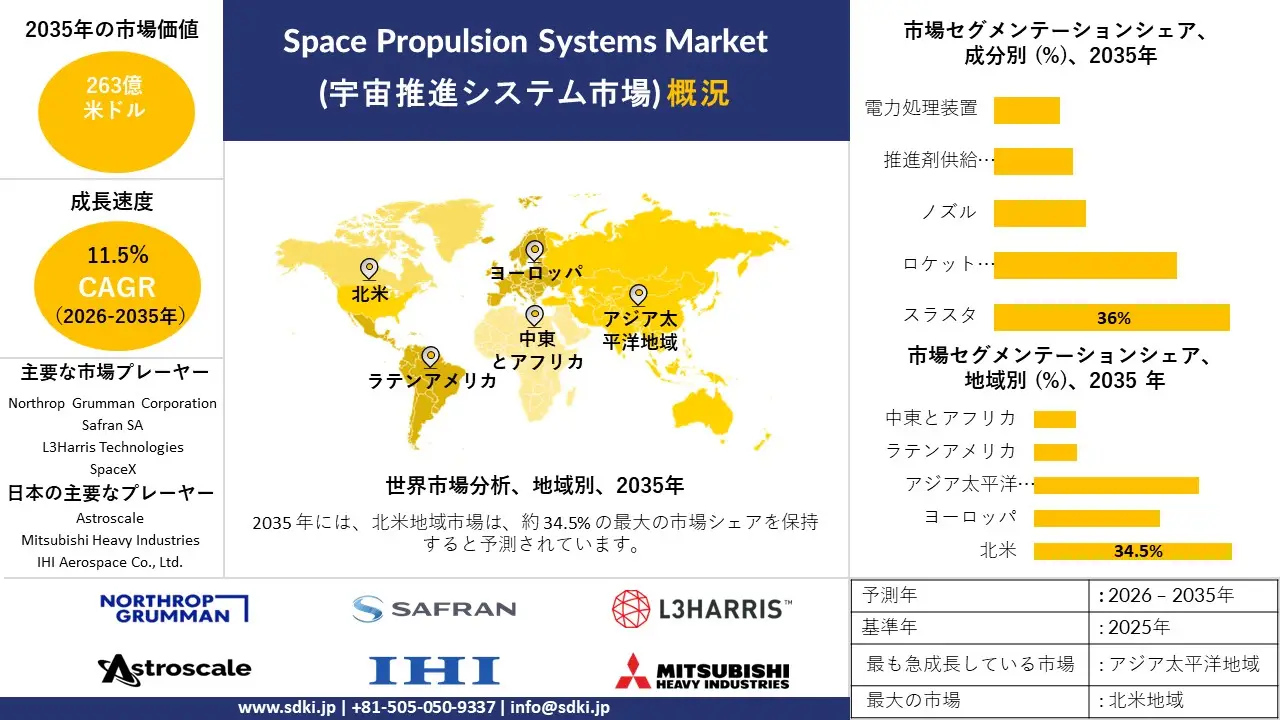

宇宙推進システム市場規模

2026―2035年のSpace Propulsion Systems Market(宇宙推進システム市場) の規模はどのくらいですか?

Space Propulsion Systems Market(宇宙推進システム市場) に関する当社の調査レポートによると、同市場は予測期間(2026―2035年)の間に複利年間成長率(CAGR)11.5%で成長すると予想されています。将来的には、市場規模は263億米ドルに達する見込みです。しかし、当社の調査アナリストによると、基準年の市場規模は96億米ドルでしました。

Space Propulsion Systems Market(宇宙推進システム市場) において、市場シェアの面でどの地域が優位を占めると予想されますか?

宇宙推進システムに関する当社の市場調査によると、北米市場は予測期間中、約34.5%という圧倒的な市場シェアを維持すると予想されます。一方、アジア太平洋地域市場は今後数年間で有望な成長機会を示すと見込まれています。この成長は主に、経済的・人口動態的要因、技術導入、規制環境、そして業界の触媒となる要素によるものです。

宇宙推進システム市場分析

宇宙推進システムとは何ですか?

宇宙推進システムとは、推力を発生させることで宇宙船や人工衛星を加速させるために使用される機構及び技術のことであります。 これらのシステムは、推力と比推力によって特徴づけられます。

Space Propulsion Systems Market(宇宙推進システム市場) における最近の傾向は何ですか?

当社のSpace Propulsion Systems Market(宇宙推進システム市場) 分析調査レポートによると、以下の市場傾向と要因が市場成長の主要な推進力として貢献すると予測されています。

- 公的研究開発・探査予算 ―宇宙

研究・探査プログラムへの継続的な世界的投資は、先進的な宇宙推進システム及び打ち上げ推進システムの開発パイプラインを強化しています。

例えば、NASAの2025会計年度予算要求では、総額254億米ドルのうち、宇宙技術に11.8億米ドル、深宇宙探査システムに76.2億米ドルが割り当てられており、高度な上段ロケットや宇宙空間での推進能力を必要とする技術成熟化や、有人探査及びロボット探査アーキテクチャへの資金提供が行われます。

さらに、NASAの機関ファクトシートでは、「統合型月面探査から火星探査までを含むミッション能力と技術の向上」のための技術研究開発に12億米ドルを投じることを改めて表明しており、これは従来から電気推進や高出力システムのロードマップ活動を包含するものであり、世界的な先進推進技術の革新と展開を加速させるものであります。

- 企業レベルでの推進システム規模拡大–

上場企業の提出書類によると、推進システムの受注残と生産能力の拡大が見られ、エンジン、モーター、スラスタの再納入につながっている。ノースロップ・グラマンは、過去最高の915億米ドルの受注残を報告した。 Bは、2025年までの一貫したオーガニック売上高成長見通しを示しており、これは国家計画や探査機で使用される固体ロケットブースターを含む、同社の推進システム事業全体における需要を裏付けるものであります。

さらに、L3Harris TechnologiesはAerojet Rocketdyneを買収した後、2024年の収益を213億米ドルと報告した。 Bは340億米ドル B 記録的な受注残高と専用の Aerojet Rocketdyne セグメントの収益が Q1 - 2025 で開示されたため、RL10/RS - 25 及び戦略的な推進ラインの持続的な受注が堅調な市場拡大につながることを示しています。

Space Propulsion Systems Market(宇宙推進システム市場) は、日本の市場参入企業にどのようなメリットをもたらしますか?

SDKIの市場展望によると、日本のSpace Propulsion Systems Market(宇宙推進システム市場) は、政府による支援投資と宇宙活動の活発化を背景に、世界市場で力強い成長を遂げると予測されています。当社の市場調査レポートによると、2024年には日本の宇宙船運用会社によって14基の衛星が打ち上げられており、これは日本の宇宙活動の活発化を示しています。さらに、世界経済フォーラムのレポートでは、日本の宇宙産業の規模は4兆円であり、2030年代初頭には8兆円に拡大すると予測されています。推進システムは、この成長を支える上で重要な役割を果たすです。先進的な推進技術により、日本の市場プレーヤーは衛星の運用効率を高め、ミッション寿命を延ばし、正確な軌道制御を実現できるようになります。推進技術の進歩により、日本の市場プレーヤーは競争力を強化し、グローバルパートナーシップを構築し、政府の野心的な宇宙開発目標に直接貢献することができます。

Space Propulsion Systems Market(宇宙推進システム市場) に影響を与える主な制約要因は何ですか?

厳しい環境・安全規制は、世界のSpace Propulsion Systems Market(宇宙推進システム市場) の成長を阻害する大きな要因となる可能性があります。従来の化学推進システムは、保管、取り扱い、打ち上げ作業中にリスクを伴う危険な推進剤を使用しています。環境に優しい推進剤の採用を求める圧力が高まるにつれ、移行の複雑さとコストが増加し、市場の成長ペースが鈍化する可能性があります。

サンプル納品物ショーケース

- 調査競合他社と業界リーダー

- 過去のデータに基づく予測

- 会社の収益シェアモデル

- 地域市場分析

- 市場傾向分析

宇宙推進システム市場レポートの洞察

Space Propulsion Systems Market(宇宙推進システム市場) の将来展望はどうなっていますか?

SDKI Analyticsの専門家によると、Space Propulsion Systems Market(宇宙推進システム市場) の世界シェアに関するレポートの洞察は以下のとおりです。

|

レポートのインサイト |

|

|

2026―2035年の複利年間成長率(CAGR) |

11.5% |

|

2025年の市場価値 |

96億米ドル |

|

2035年の市場価値 |

263億米ドル |

|

過去のデータ共有 |

過去5年間から2024年まで |

|

未来予測完了 |

2035年までの今後10年間 |

|

ページ数 |

200+ページ |

出典: SDKI Analytics専門家による分析

Space Propulsion Systems Market(宇宙推進システム市場) はどのように分割されていますか?

当社は、Space Propulsion Systems Market(宇宙推進システム市場) の見通しに関連する様々なセグメントにおける需要と機会を説明する調査を実施しました。市場は、推進方式別、プラットフォーム別、成分別、エンドユーザー別にセグメントに分割されています。

Space Propulsion Systems Market(宇宙推進システム市場) は、成分別にどのように分割されていますか?

成分別に基づいて、Space Propulsion Systems Market(宇宙推進システム市場) はスラスタ、ロケットモーターズ、ノズル、推進剤供給システム、電力処理装置に分割され、スラスタは2035年までに36%という最大の市場シェアを占めると予想されます。

当社の市場見通し及び調査報告書では、衛星の移動、軌道制御、打ち上げ推進において重要な役割を担うスラスタとロケットモーターが市場を牽引すると予測しています。衛星打ち上げの増加に伴い、これらの部品の需要も高まっています。

ヨーロッパ宇宙機関によると、現在6000基以上の衛星が高度500―600メートルの間に位置し、宇宙活動の著しい成長を示しています。このトレンドは、先進的な推進コンポーネントの採用拡大も後押ししています。

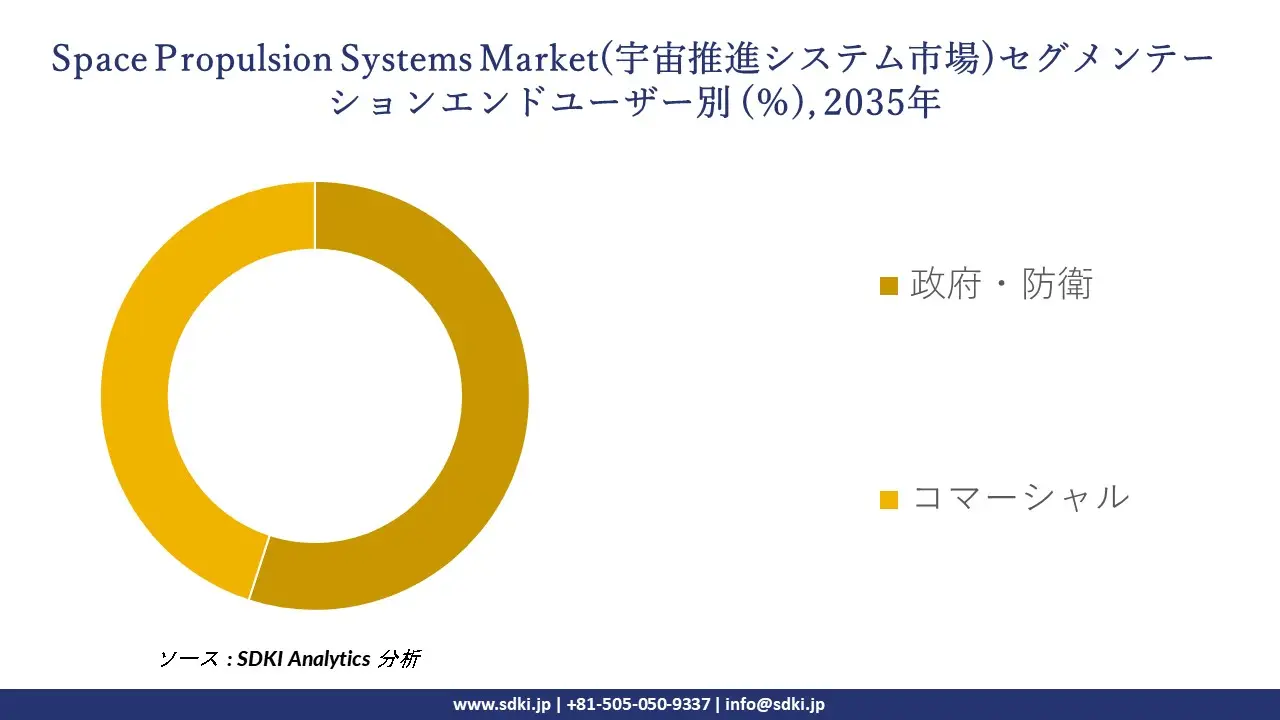

Space Propulsion Systems Market(宇宙推進システム市場) は、エンドユーザー別にどのように分割されていますか?

エンドユーザー別に基づいて、Space Propulsion Systems Market(宇宙推進システム市場) は、政府・防衛、コマーシャルに分割されます。当社の市場見通し及び調査レポートでは、宇宙探査、衛星プログラム、国家安全保障ミッションへの多額の支出により、政府・防衛が市場シェアの55%を占め、市場を牽引すると予測しています。

宇宙機関は先進的な推進技術への投資に注力しています。NASAの2023年の調査報告書によると、米国政府は2024年にNASAに約254億米ドルを割り当てた。これは研究と宇宙ミッションを支援するためのものであります。さらに、民間セクターの参加増加に伴い、商業分野も着実に成長しています。

以下に、Space Propulsion Systems Market(宇宙推進システム市場) に適用されるセグメントの一覧を示します。

|

親セグメント |

市場サブセグメント |

|

推進方式別 |

|

|

プラットフォーム別 |

|

|

成分別 |

|

|

エンドユーザー別 |

|

出典: SDKI Analytics専門家による分析

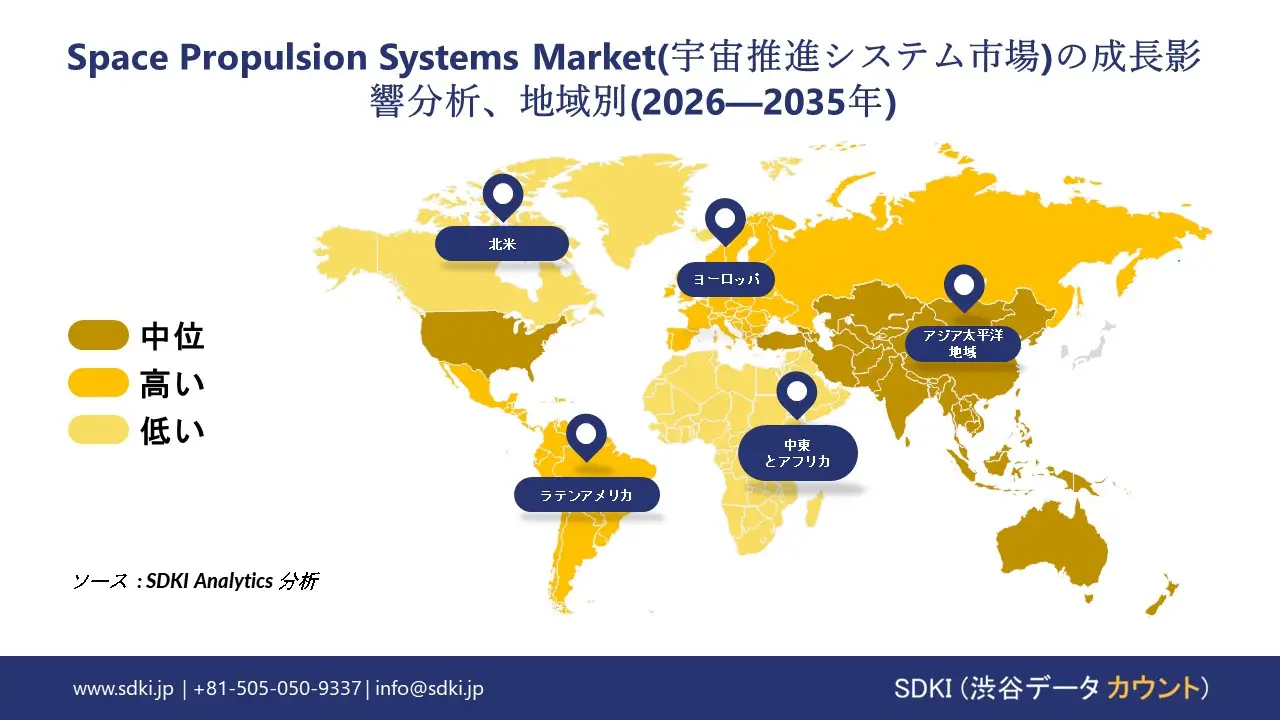

Space Propulsion Systems Market(宇宙推進システム市場) の傾向分析と将来予測:地域別市場概況

アジア太平洋地域のSpace Propulsion Systems Market(宇宙推進システム市場) の市場調査と分析によると、同地域は予測期間を通じて複利年間成長率(CAGR)15.2%で世界市場最速の成長を記録すると予測されています。同地域における宇宙ミッションの増加が、地域市場の成長を牽引しています。中華人民共和国国務院の報告によると、2023年には中国で約67回の宇宙打ち上げミッションが実施されました。これは、衛星コンステレーションの拡大と深宇宙探査に対する中国の強い取り組みを示しています。各ミッションには高度な推進システムが必要であり、アジア太平洋地域全体でイノベーションと生産が促進されています。記録的な打ち上げ回数は、政府支援プログラムがアジア太平洋地域における信頼性と効率性に優れた推進技術への需要を加速させていることを示しています。

SDKI Analyticsの専門家は、Space Propulsion Systems Market(宇宙推進システム市場) に関するこの調査レポートのために、以下の国と地域を調査しました。

|

地域 |

国 |

|

北米 |

|

|

ヨーロッパ |

|

|

アジア太平洋地域 |

|

|

ラテンアメリカ |

|

|

中東及びアフリカ |

|

出典: SDKI Analytics専門家による分析

北米におけるSpace Propulsion Systems Market(宇宙推進システム市場) の市場実績はどのようなものですか?

SDKIの市場調査アナリストは、北米のSpace Propulsion Systems Market(宇宙推進システム市場) が予測期間を通じて収益シェア34.5%で世界市場を牽引すると予測していることを明らかにしました。市場の成長は、政府による支援投資によって支えられています。米国航空宇宙局(NASA)の報告によると、米国政府は248.75億米ドルの予算を割り当てています。 2024年には数十億ドルが投じられる予定であり、これは宇宙探査に対する政府の強力な支援を示しています。この資金は、アルテミス計画、オリオン計画、スペース・ローンチ・システム(SLS)などのプログラムにおける推進システムの開発を推進しています。先進的な推進技術に重点を置くことで、この予算は有人月探査ミッション、貨物輸送、そして将来の火星探査のための信頼性の高いシステムを確保し、推進力を北米の宇宙能力拡大の中心的な原動力としています。

宇宙推進システム調査の場所

北米(米国およびカナダ)、ラテンアメリカ(ブラジル、メキシコ、アルゼンチン、その他のラテンアメリカ)、ヨーロッパ(英国、ドイツ、フランス、イタリア、スペイン、ハンガリー、ベルギー、オランダおよびルクセンブルグ、NORDIC(フィンランド、スウェーデン、ノルウェー) 、デンマーク)、アイルランド、スイス、オーストリア、ポーランド、トルコ、ロシア、その他のヨーロッパ)、ポーランド、トルコ、ロシア、その他のヨーロッパ)、アジア太平洋(中国、インド、日本、韓国、シンガポール、インドネシア、マレーシア) 、オーストラリア、ニュージーランド、その他のアジア太平洋地域)、中東およびアフリカ(イスラエル、GCC(サウジアラビア、UAE、バーレーン、クウェート、カタール、オマーン)、北アフリカ、南アフリカ、その他の中東およびアフリカ

競争力ランドスケープ

SDKI Analyticsの調査員によると、Space Propulsion Systems Market(宇宙推進システム市場) の見通しは、大企業と中小企業といった規模の異なる企業間の市場競争により、分割されます。調査報告書によると、市場参加者は、製品や技術の発表、戦略的提携、協力、買収、事業拡大など、あらゆる機会を活用して、市場全体の見通しにおいて競争優位性を獲得しようとしています。

Space Propulsion Systems Market(宇宙推進システム市場) で事業を展開する主要なグローバル企業はどこですか?

当社の調査報告書によると、世界のSpace Propulsion Systems Market(宇宙推進システム市場) の成長において重要な役割を担う主要企業には、Northrop Grumman Corporation、 Safran SA、 SpaceX、 L3Harris Technologies、 Airbus Defence and Spaceなどが含まれます。

Space Propulsion Systems Market(宇宙推進システム市場) で競合する主要な日本企業はどこですか?

市場見通しによると、日本のSpace Propulsion Systems Market(宇宙推進システム市場) における上位5社は、Space BD Inc.、 Astroscale、 AstroX Inc.、 Mitsubishi Heavy Industries (MHI)、 IHI Aerospace Co. Ltd.などであります。

この市場調査レポートには、世界のSpace Propulsion Systems Market(宇宙推進システム市場) 分析調査レポートにおける主要企業の詳細な競合分析、企業プロファイル、最近の傾向、及び主要な市場戦略が含まれています。

Space Propulsion Systems Market(宇宙推進システム市場) における最新のニュースや傾向は何ですか?

- 2025年4月 - Nippon Shokubai Co. Ltd.は、北九州市と、商標名「IONEL」で販売されるLiFSI (リチウムビス(フルオロスルホニル)イミド)の新生産拠点を設立するための立地協定を締結しました。協定は北九州市役所で正式に締結されました。

- 2026年3月 - 軌道上操縦用の先進推進システムを開発するドイツ拠点のISPTechは、運用中の宇宙ミッション向けに同社の無毒性推進ソリューションの展開を加速させるため、シード資金調達ラウンドで5.5百万ユーロの資金調達に成功した。

宇宙推進システム主な主要プレーヤー

主要な市場プレーヤーの分析

日本市場のトップ 5 プレーヤー

目次

宇宙推進システムマーケットレポート

関連レポート

よくある質問

- 2020ー2024年

- 2026-2035年

- 必要に応じて日本語レポートが入手可能

品質と信頼の証