- 2020ー2024年

- 2026-2035年

- 必要に応じて日本語レポートが入手可能

品質と信頼の証

固定翼VTOL無人航空機市場規模

2026―2035年のFixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)の規模はどのくらいですか?

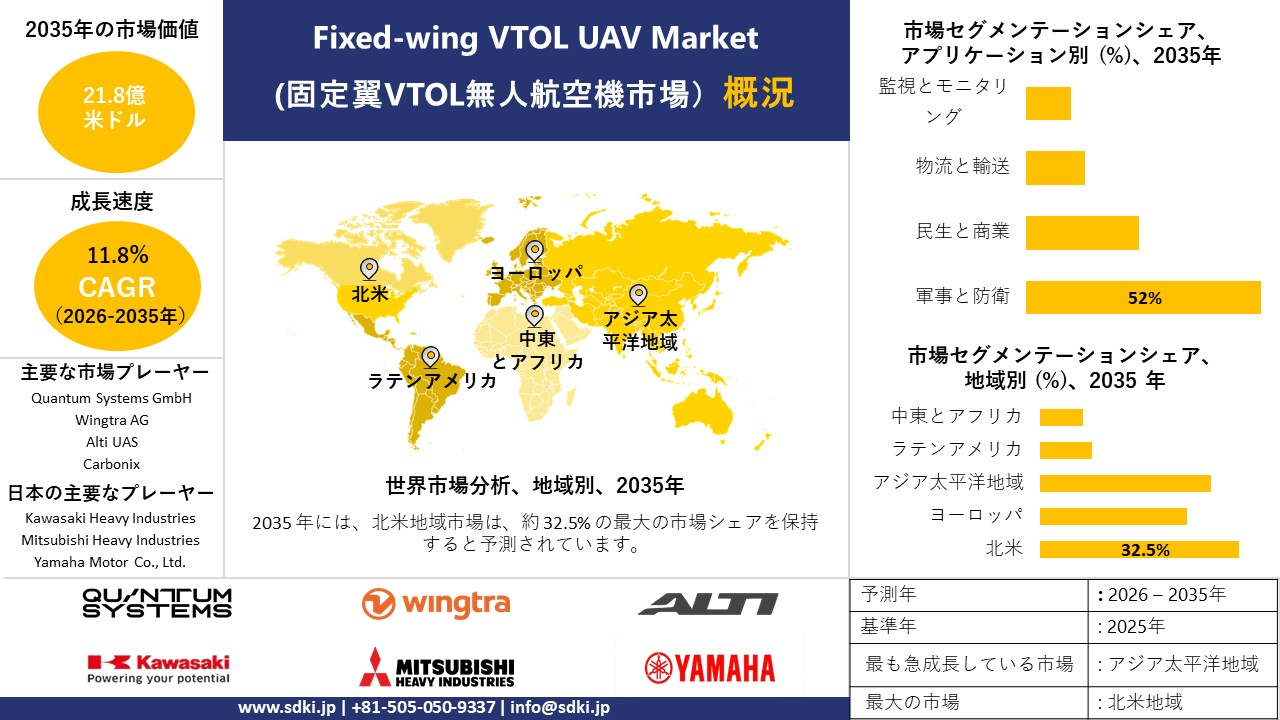

Fixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)に関する弊社の調査レポートによると、同市場は予測期間2026―2035年中に複利年間成長率(CAGR)11.8%で成長すると予想されています。来年には、市場規模は21.8億米ドルに達する見込みです。ただし、弊社の調査アナリストによると、基準年の市場規模は7.1億米ドルでした。

Fixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)において、市場シェアの面でどの地域が優位を占めると予想されますか?

固定翼VTOL無人航空機に関する弊社の市場調査によると、北米市場は予測期間中、約32.5%という圧倒的な市場シェアを維持すると予想されます。一方、アジア太平洋地域市場は今後数年間で有望な成長機会を示すと見込まれています。この成長は主に、進行中の防衛近代化と商用ドローンアプリケーションの拡大によるものです。

固定翼VTOL無人航空機市場分析

固定翼VTOL無人航空機とは何ですか?

固定翼VTOL無人航空機はハイブリッド航空機である。マルチローター機のホバリング能力と滑走路不要の飛行能力に、従来の飛行機の長距離・高速飛行における空力効率性を組み合わせたものであります。

Fixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)における最近の傾向は何ですか?

弊社のFixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)分析調査レポートによると、以下の市場傾向と要因が市場成長の主要な推進力として貢献すると予測されています。

- 規制の調和とBVLOSの拡大-

弊社の調査レポートによると、BVLOSミッションの採用増加に伴い、世界的に固定翼VTOL無人航空機プラットフォームの需要が高まっています。例えば、FAAのBEYONDプログラムでは、8つの主要参加企業で合計70,563回の飛行が行われ、そのうち48,383回がBVLOS飛行でした。 2024年のFAA再承認法に基づき、2025年に2件の 13、 2025年のページでは、実際のミッションを定量化し、固定翼VTOLの強みに直接結びつく、線状インフラの点検や公共の安全といったユースケースを強調しています。

これに加えて、EU U - space ルールの実施において、EASA は統合された Easy Access ルールと継続的な AMC/GM の更新を提供しており、USSP 認証は加盟国全体で再現可能な運用に必要なサービス レイヤーを開始します。ミッション タイムの増加により、商業オペレーターはBVLOS 飛行、長距離飛行、滑走路なしでの離着陸が可能な固定翼 VTOL プラットフォームに傾倒しています。

- 世界の調達及び輸出チャネル–固定-

翼VTOLシステムを大規模に購入するための世界のな資金調達メカニズムが現在整備されています。例えば、12月には 8、 2025年、エアロバイロメントは5年間で874.26 百万米ドルの契約を発表しました。 数百万ドルの米陸軍対外軍事販売IDIQリストJUMP 同盟国調達の対象となるシステムのうち20機種は、米国政府の契約と、固定翼VTOL ISRを含むOEMポートフォリオを組み合わせたものであります。

ヨーロッパでは、エアロバイロメントは181百万米ドルを計上しました。 46.6百万米ドル JUMPの数百万ドル規模の契約 これにより、 20のプログラムが構築され、従来の滑走路依存型システムを滑走路非依存型のVTOL ISRに置き換える複数年調達が実現します。

Fixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)は、日本の市場参入企業にどのようなメリットをもたらすのは何ですか?

Fixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)は、日本企業が抱える重要な課題の解決に役立つ可能性がある。日本は労働力不足に直面しており、遠隔地や山間部が多くなります。調査報告書にも指摘されていますように、ドローン規制は厳しく、イノベーションの妨げとなっています。固定翼VTOL無人航空機は長距離輸送が可能で、災害対応にも役立つ。これは離島にとって特に有用だ。経済複雑性観測所(OEC)の報告書によると、日本は2024年に95.1百万米ドル相当のドローンを輸入した。

これは、外国技術への依存度が高く、国内生産の必要性が高まっていますことを示しています。政府は改正法に基づきレベル4の目視外飛行(BVLOS)を許可しており、これは自律型ドローンの利用を促進するとともに、市場の見通しを改善しています。Mitsubishi Heavy IndustriesやKawasaki Heavy Industriesなどの企業は、無人航空機(UAV)技術の開発に取り組んでおり、防衛及び物流アプリケーションに重点を置いています。これらのドローンは、輸入を減らし、日本の航空宇宙産業を活性化させる可能性を秘めています。

Fixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)に影響を与える主な制約要因は何ですか?

高額な購入費用と維持費用は、世界のFixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)の成長にとって大きな脅威となる可能性があります。航続距離と積載能力に優れた固定翼VTOL無人航空機は、購入費用と維持費用が高額であります。中小企業や地方自治体はこうしたシステムを導入することが難しく、世界市場への普及を阻害する要因となっています。

サンプル納品物ショーケース

- 調査競合他社と業界リーダー

- 過去のデータに基づく予測

- 会社の収益シェアモデル

- 地域市場分析

- 市場傾向分析

固定翼VTOL無人航空機市場レポートの洞察

Fixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)の将来展望はどうですか?

SDKI Analyticsの専門家によると、Fixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)の世界シェアに関するレポートの洞察は以下のとおりです。

|

レポートの洞察 |

|

|

2026-2035年の CAGR |

11.8% |

|

2025年の市場価値 |

7.1億米ドル |

|

2035年の市場価値 |

21.8億米ドル |

|

過去のデータ共有 |

過去5年間から2024年まで |

|

将来予測 |

2035年までの今後10年間 |

|

ページ数 |

200ページ |

ソース: SDKI Analytics 専門家分析

Fixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)はどのようにセグメント化されていますか?

弊社は、Fixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)の見通しに関連する様々なセグメントにおける需要と機会を説明する調査を実施しました。市場は、アプリケーション別、推進方式別、ペイロード容量別、航続距離別、航続時間別、VTOL方式別に分割されています。

Fixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)は、アプリケーション別にどのように区分されていますか?

弊社の市場分析によると、Fixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)は、アプリケーション別に基づいて、軍事と防衛、民生と商業、物流と輸送、監視とモニタリングに分割されています。国境警備や偵察任務への需要から、軍事アプリケーションが市場を牽引し、52%の市場シェアを占めると予想されます。

地図作成や農業分野における利用拡大に伴い、民生商業アプリケーションも増加しています。さらに、遠隔地におけるラストマイル配送のニーズの高まりにより、物流分野での利用も増加しています。連邦航空局(FAA)の調査報告によると、2024年には米国で800,000機以上のドローンが登録されており、様々なアプリケーションで急速に普及が進んでいますことが示されています。

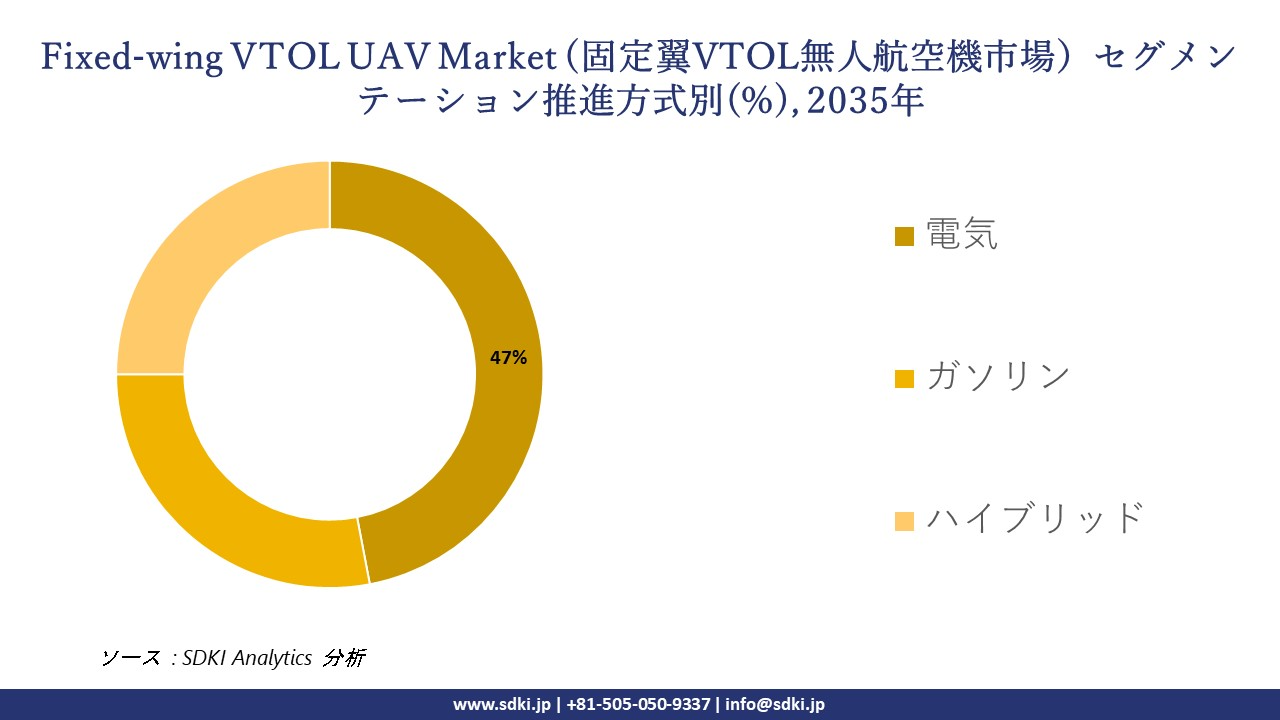

Fixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)は、推進方式別によってどのように区分されるのでしょうか?

推進方式別に基づいて、電気、ガソリン、ハイブリッドに分割されています。電気UAVは、低騒音かつ排出ガスゼロであることから広く普及しており、予測期間中に47%という最大の市場シェアを占めると予想されています。ガソリンは航続距離が長く、ハイブリッドは両方の利点を兼ね備え、より長時間のミッションに対応できます。

弊社の市場見通しによると、多くの企業が電気システムやハイブリッドシステムへの移行を進めています。国際エネルギー機関の調査報告書によると、2023年には世界の電気自動車の販売台数が14百万台近くに達し、急速な電動化の傾向が見られ、これが無人航空機(UAV)の電動推進市場を後押ししています。

以下に、Fixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)に適用されるセグメントの一覧を示します。

|

市場セグメント |

市場サブセグメント |

|

アプリケーション別 |

|

|

推進方式別 |

|

|

ペイロード容量別 |

|

|

航続距離別 |

|

|

航続時間別 |

|

|

VTOL方式別 |

|

ソース: SDKI Analytics 専門家分析

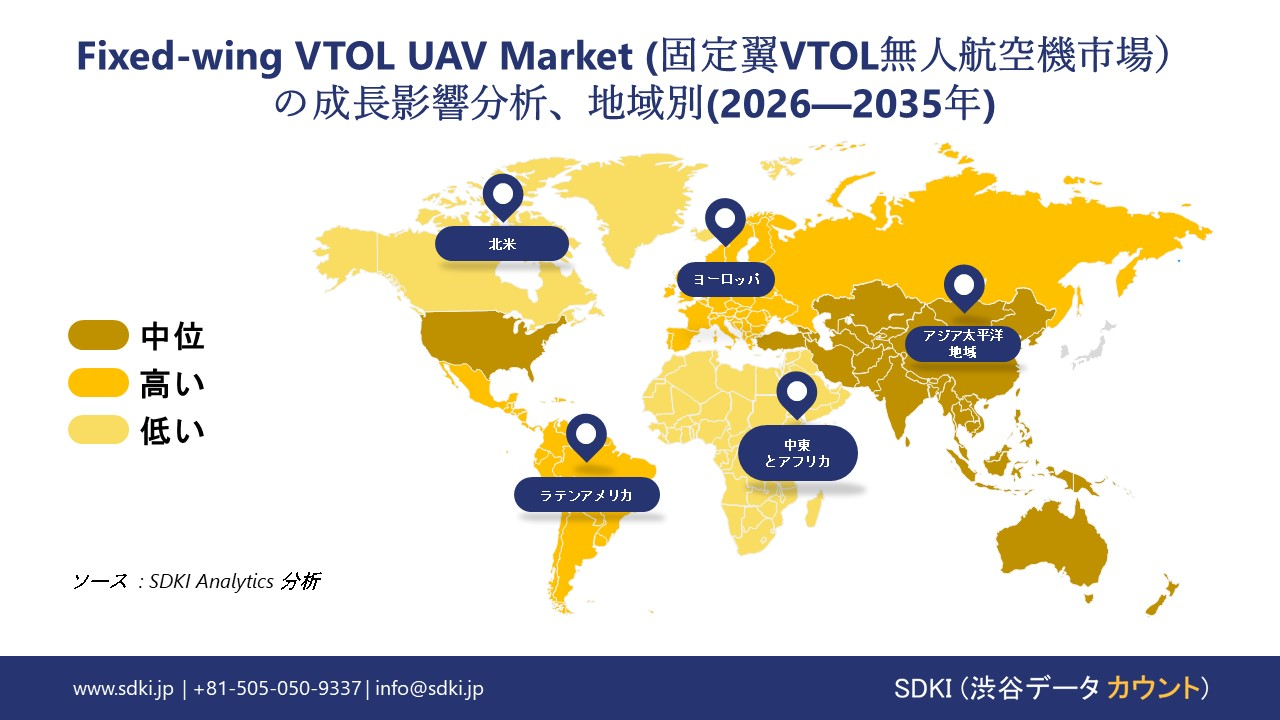

Fixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)の傾向分析と将来予測:地域別市場概況

アジア太平洋地域のFixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)は、予測期間中に複利年間成長率(CAGR)16.4%で、世界市場で最も急速に成長する地域になると予想されています。地域全体の政府による支援策が、この地域市場の成長を後押ししています。

インドの報道情報局の報告によると、2023年に承認され、1261クロールインドルピー(2023~24年度から2025~26年度)の予算が計上されたインドの「Namo Drone Didi」計画は、アジア太平洋地域における無人航空機(UAV)の成長を直接的に支援していますことが判明した。

女性自助グループにドローンをレンタルサービスとして提供することで、農家は手頃な価格で最新の散布技術を利用できるようになります。この取り組みは作物の効率を高め、資源の無駄を削減し、農村部の女性のエンパワーメントを促進するため、農業はこの地域における固定翼VTOL無人航空機の普及を強力に推進する原動力となります。

SDKI Analyticsの専門家は、Fixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)に関するこの調査レポートのために、以下の国と地域を調査しました。

|

地域 |

国 |

|

北米 |

|

|

ヨーロッパ |

|

|

アジア太平洋地域 |

|

|

ラテンアメリカ |

|

|

中東とアフリカ |

|

ソース: SDKI Analytics 専門家分析

北米におけるFixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)の市場実績はどうですか?

SDKIの市場調査アナリストは、北米のFixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)が予測期間を通じて世界市場において支配的な地位を占め、市場シェアは32.5%になると予測していますことを明らかにしました。

地域全体で法執行機関による無人航空機(UAV)の導入が拡大していますことが、市場の成長を後押ししています。米国司法省の報告によると、2024年には約3,273機のUAVが配備され、前年比で46.9%増加した。

この急速な成長は、法執行機関が監視、モニタリング、緊急対応において無人航空機(UAV)への依存度を高めていますことを示しています。こうした政府主導の運用拡大は、北米における公共安全セキュリティ分野全体での固定翼VTOL(垂直離着陸)UAVの導入を直接的に促進します。

固定翼VTOL無人航空機調査の場所

北米(米国およびカナダ)、ラテンアメリカ(ブラジル、メキシコ、アルゼンチン、その他のラテンアメリカ)、ヨーロッパ(英国、ドイツ、フランス、イタリア、スペイン、ハンガリー、ベルギー、オランダおよびルクセンブルグ、NORDIC(フィンランド、スウェーデン、ノルウェー) 、デンマーク)、アイルランド、スイス、オーストリア、ポーランド、トルコ、ロシア、その他のヨーロッパ)、ポーランド、トルコ、ロシア、その他のヨーロッパ)、アジア太平洋(中国、インド、日本、韓国、シンガポール、インドネシア、マレーシア) 、オーストラリア、ニュージーランド、その他のアジア太平洋地域)、中東およびアフリカ(イスラエル、GCC(サウジアラビア、UAE、バーレーン、クウェート、カタール、オマーン)、北アフリカ、南アフリカ、その他の中東およびアフリカ

競争力ランドスケープ

SDKI Analyticsの調査者によると、Fixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)の見通しは、大企業と中小企業といった規模の異なる企業間の市場競争により、細分化されています。調査報告書によると、市場参加者は、製品や技術の発表、戦略的パートナーシップ、コラボレーション、買収、事業拡大など、あらゆる機会を活用して、市場全体の見通しにおいて競争優位性を獲得しようとしています。

Fixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)で事業を展開しています主要な世界の企業はどれですか?

弊社の調査報告書によると、世界のFixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)の成長において重要な役割を担う主要企業には、Quantum Systems GmbH、Wingtra AG、Alti UAS、Carbonix、IdeaForge Technologyなどが含まれます。

Fixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)で競合する主要な日本企業はどれですか?

市場見通しによると、日本のFixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)の上位5社は、Yamaha Motor Co., Ltd.、ACSL Ltd.、Aerosense Inc.、Kawasaki Heavy Industries、 Mitsubishi Heavy Industriesなどであります。

この市場調査レポートには、世界のFixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)分析調査レポートにおける主要企業の詳細な競合分析、企業プロファイル、最近の傾向、及び主要な市場戦略が含まれています。

Fixed-wing VTOL UAV Market (固定翼VTOL無人航空機市場)における最新のニュースや傾向は何ですか?

- 2025年7月、 STMはIDEF 2025において、最新の固定翼VTOL無人航空機システムを発表しました。長時間の飛行時間、多様な弾薬への対応、そして高いペイロード容量を備えたSTM VTOLは、軍事及び民間のミッションニーズの両方に対応できる体制を整えています。

- 2026年3月、 ANA Holdings Incは、垂直離着陸(VTOL)固定翼機を活用した日本全国における広域測量と検査サービスの展開を検討するため、ウィングトラ社と覚書(MOU)を締結した。

固定翼VTOL無人航空機主な主要プレーヤー

主要な市場プレーヤーの分析

日本市場のトップ 5 プレーヤー

目次

固定翼VTOL無人航空機マーケットレポート

関連レポート

よくある質問

- 2020ー2024年

- 2026-2035年

- 必要に応じて日本語レポートが入手可能

品質と信頼の証