- 2020ー2024年

- 2026-2035年

- 必要に応じて日本語レポートが入手可能

品質と信頼の証

舶用推進エンジン市場規模

2026―2035年の舶用推進エンジン市場の市場規模はどのくらいですか?

弊社の舶用推進エンジン市場調査レポートによると、市場は予測期間2026―2035年において約5.8%の複利年間成長率(CAGR)で成長すると予想されています。来年には、世界市場は約423億米ドルに達すると予想されています。しかし、弊社の調査アナリストによると、基準年である2025年の市場規模は約241億米ドルとされています。

市場シェアの観点から、舶用推進エンジン市場を支配すると予想される地域はどれですか?

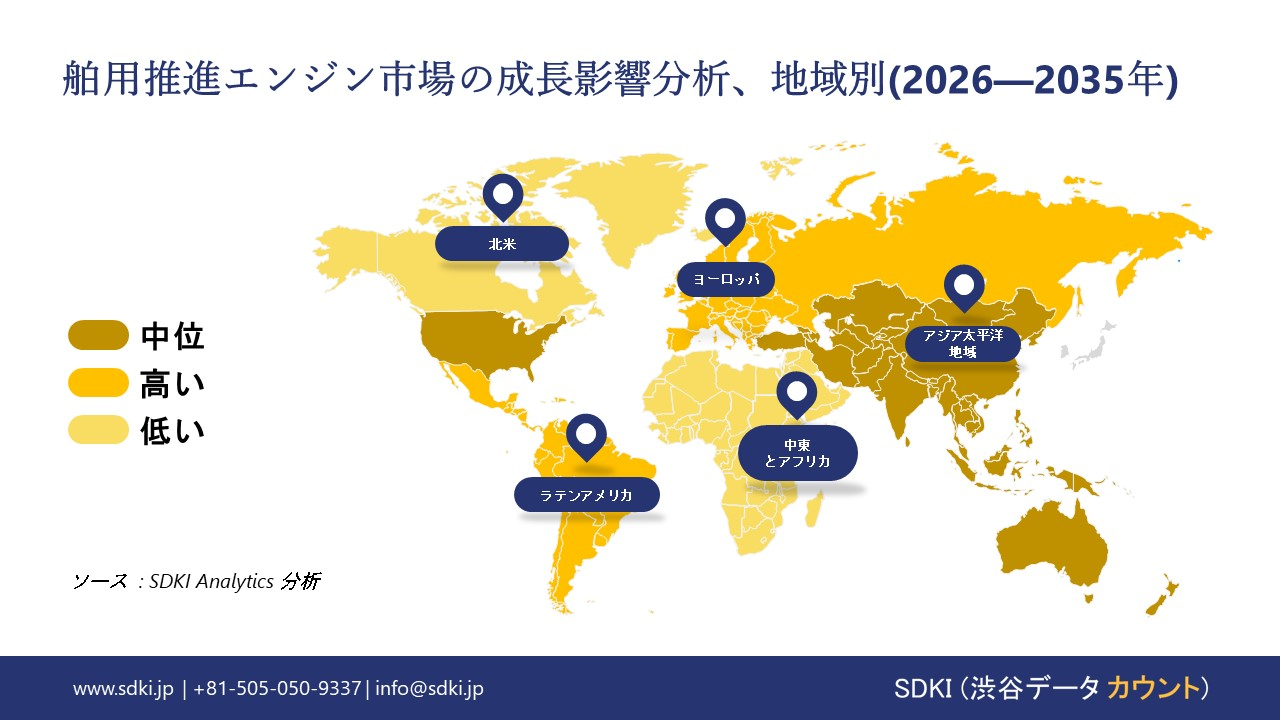

舶用推進エンジン業界に関する弊社の市場調査によると、アジア太平洋地域(APAC)は予測期間を通じて約54.5%の市場シェアを維持し、その優位性を強固なものにすると予想されています。同時に、アジア太平洋地域は最も高いCAGRを示すと予測されており、今後数年間で最大の成長機会が見込まれます。この成長加速は、主に主要な地域要因、すなわち大手船会社による積極的な船隊近代化と拡張、政府主導による港湾と海事インフラへの多額の投資、そして厳格な世界的排出規制を満たすための次世代グリーン推進技術(LNG、メタノール、アンモニア燃料エンジンなど)の開発と導入に向けた業界の重点的な転換の結果です。

舶用推進エンジン市場分析

舶用推進エンジンとは何ですか?

舶用推進エンジンは、船舶を水中で推進させるための推進力を生み出す機械システムまたは動力装置です。船舶の推進システムの中核を成し、燃料、電気、その他のエネルギー源から得られるエネルギーを回転力に変換し、プロペラ、ウォータージェット、その他の推進力発生装置に伝達します。

舶用推進エンジン市場の最近の傾向は何ですか?

弊社の舶用推進エンジン市場分析調査レポートによると、以下の市場傾向と要因が市場成長の中核的な原動力として貢献すると予測されています。

- 国際海事機関(IMO)の温室効果ガス(GHG)戦略と炭素強度規制 –

IMOの2023年改訂版GHG戦略は、国際海運業界に対し、拘束力のある、より厳格な目標を設定しており、2050年頃までに温室効果ガス排出量を実質ゼロにするというコミットメントも含まれています。この戦略は、炭素強度指標(CII)や既存船舶エネルギー効率指数(EEXI)といった短期的な指標を通じて施行され、船舶を評価し、運航改善を義務付けています。この規制では、主推進機関と補助推進機関の効率が重要な遵守要素となっています。船主は、既存のエンジンを省エネ技術に改造するか、より低炭素な代替エンジンに交換することが義務付けられており、これは世界市場での運航継続性維持に役立ちます。

- グリーン海洋技術開発への政府資金と補助金 –

米国、EU、中国などの先進国及び発展途上国の政府は、国家の気候目標の達成に向け、次世代推進技術の研究、開発、導入に直接資金を提供しています。たとえば、ホライズンヨーロッパイノベーションファンドは、水素燃料電池やアンモニア燃料エンジンの開発と導入などのプロジェクトを推進しています。ヨーロッパ委員会は、10年間で約2.2百万トンの再生可能水素を生産し、15百万トン以上のCO₂排出を削減できると期待される15の再生可能水素生産プロジェクトを選定したことを発表しました。同様に、米国の環境保護庁(EPA)のディーゼル排出削減法(DERA)プログラムは、市場を促進するクリーンなモデルに船舶エンジンを交換するための助成金を提供しています。

舶用推進エンジン市場における舶用推進エンジンの輸出に関して、日本の地元企業はどのような利益を得るのですか?

舶用推進エンジンは、日本の市場プレーヤーに輸出バリューチェーン全体にわたる多くの機会を提供しています。日本は2023年に約456百万米ドル相当の船舶推進ディーゼルエンジンを輸出し、このクラスの船舶機器の世界有数のサプライヤーとなりました。輸出先は多様化しており、中国、東南アジア、EUは常に最大の輸入国にランクインしており、単一市場リスクに対する耐性を高めています。さらに、2018年12月に日本が発効したCPTPPは、参加国の船舶機械に対する関税を撤廃し、RCEPはASEAN造船拠点への特恵アクセスを向上させます。同様に、JETROの船舶機器輸出支援プログラム(2023―2025年)は、中小企業の輸出準備を強化するための資金調達と海外ビジネスマッチングを提供します。Mitsui E&S Group 2024統合報告書などの企業開示情報では、アジアの造船所向けのデュアル燃料推進システムに焦点を当てた舶用エンジンが主要輸出事業として挙げられています。また、経済産業省製造業実態調査報告書(2024年版)によると、輸出志向の機械メーカーは稼働率の向上を報告しており、2027―2030年にかけての日本の中期的な輸出成長を後押しする要因となっています。

舶用推進エンジン市場に影響を与える主な制約は何ですか?

業界における義務的なグリーン移行に伴う莫大な資本コストと財務リスクは、市場における大きな制約要因となっています。規制に適合した新しいエンジンの開発、認証、そして量産には、莫大な先行研究開発投資が必要です。 船主にとって、既存の船舶を改造したり、このような高度な推進力を備えた新造船を購入したりするための資本支出(CAPEX)は、潜在的な長期的な運用コストの削減にもかかわらず、従来のディーゼルオプションよりも大幅に高く、市場プレーヤーの運用収益に影響を与え、市場の成長を妨げます。

サンプル納品物ショーケース

- 調査競合他社と業界リーダー

- 過去のデータに基づく予測

- 会社の収益シェアモデル

- 地域市場分析

- 市場傾向分析

舶用推進エンジン市場レポートの洞察

舶用推進エンジン市場の今後の見通しはどのようなものですか?

SDKI Analyticsの専門家によると、舶用推進エンジン市場の世界シェアに関連するレポートの洞察は以下の通りです。

|

レポートの洞察 |

|

|

2026-2035年の CAGR |

5.8% |

|

2025年の市場価値 |

241億米ドル |

|

2035年の市場価値 |

423億米ドル |

|

過去のデータ共有 |

過去5年間 2024年まで |

|

将来予測 |

2035年までの今後10年間 |

|

ページ数 |

200+ページ |

ソース: SDKI Analytics 専門家分析

舶用推進エンジン市場はどのように区分されていますか?

弊社は、舶用推進エンジン市場の見通しに関連する様々なセグメントにおける需要と機会を説明する調査を実施しました。市場は、エンジンタイプ別、燃料タイプ別、推進システム別、最終用途産業別、販売チャネル別に分割されています。

舶用推進エンジン市場はエンジンタイプ別によってどのように区分されていますか?

舶用推進エンジン市場はエンジンタイプ別に基づいて、ディーゼルエンジン、ガスタービンエンジン、蒸気タービンエンジン、船外機、船内機に分割されています。調査報告書によると、ディーゼルエンジンは2025年までに46%のシェアを占めると予想されています。 2035年ディーゼル推進システムは、実証済みの信頼性、高トルク出力、そして長い運用ライフサイクルにより、世界の商用船隊の大部分を支え続けています。このサブセグメントの市場見通しは、即時の代替よりも、燃費効率に関する規制圧力によって左右されます。2023年には、国際海事機関(IMO)が 2050年頃までに国際海運からのネットゼロ排出量を目標とする改訂版GHG戦略を採択し、 2030年と2040年に暫定的な排出削減チェックポイントを設定しました。この公式の政策枠組みは、ディーゼルエンジンの継続的な導入を強化するとともに、特に貨物船とタンカー船の分野で、既存の船隊全体で効率性の向上、二重燃料の互換性、及び改造の採用を加速します。

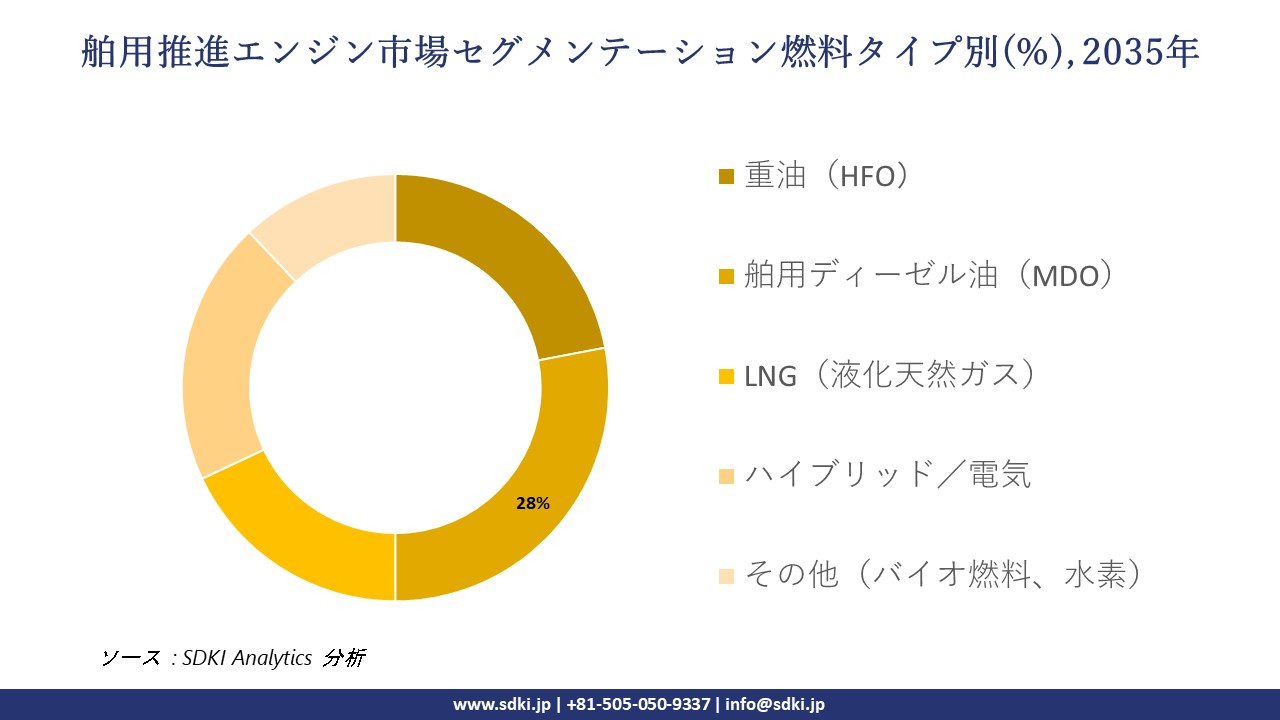

舶用推進エンジン市場は燃料タイプ別によってどのように区分されていますか?

舶用推進エンジン市場は燃料タイプ別に基づいて、重油(HFO)、舶用ディーゼル油(MDO)、LNG(液化天然ガス)、ハイブリッド/電気、その他(バイオ燃料、水素)に分割されています。調査レポートによると、舶用ディーゼル油(MDO)は 2035年までに28%のシェアを占めると予測されています。MDOは、HFOに比べて硫黄含有量が低く、既存のディーゼルエンジンプラットフォームとの互換性があるため、引き続き広く採用されています。このセグメントは、規制遵守要件と、商船やオフショア支援船を含む船舶クラス全体にわたる運用柔軟性の恩恵を受けています。燃料転換戦略は段階的な多様化に影響を与えていますが、MDOは依然として、現在の舶用推進エンジンにおいて、規制遵守に適合した実用的な燃料選択肢として機能しています。

以下は、舶用推進エンジン市場に該当するセグメントのリストです。

|

親セグメント |

サブセグメント |

|

エンジンタイプ別 |

|

|

燃料タイプ別 |

|

|

推進システム別 |

|

|

最終用途産業別 |

|

|

販売チャネル別 |

|

ソース: SDKI Analytics 専門家分析

舶用推進エンジン市場傾向分析と将来予測:地域市場展望概要

舶用推進エンジン市場はアジア太平洋地域で発展しており、予測期間中に24.8%のCAGRが予測されています。国家の海軍と沿岸警備隊の近代化と拡張プログラムは市場の成長を支えており、将来的には市場が54.5%の最大シェアを獲得するのに役立つでします。中国人民解放軍海軍(PLAN)は、従来のディーゼルやガスタービンから、先進的な船舶向けの新興の原子力及び統合電気推進まで、推進力のニーズに対応する歴史的な造船キャンペーンを継続しています。中国海軍は、2025年までに船舶を395隻、2030年までに435隻に増やす計画です。同様に、インド国防省は艦隊の近代化を進めており、新しい潜水艦、フリゲート艦、航空母艦用の推進システムが必要であり、これも舶用推進エンジンを支援しています。

SDKI Analyticsの専門家は、舶用推進エンジン市場に関するこの調査レポートのために、以下の国と地域を調査しました。

|

地域 |

国 |

|

北米 |

|

|

ヨーロッパ |

|

|

アジア太平洋地域 |

|

|

ラテンアメリカ |

|

|

中東とアフリカ |

|

ソース: SDKI Analytics 専門家分析

北米の舶用推進エンジン市場の市場パフォーマンスはどうですか?

米国国防総省による海軍力への戦略的投資は、北米市場における舶用推進エンジンの強力な市場牽引力の一つです。米海軍の30カ年造船計画は、コロンビア級弾道ミサイル潜水艦、バージニア級攻撃型潜水艦、DDG(X)次世代駆逐艦、コンステレーション級フリゲート艦など、新型艦艇の調達パイプラインを構築しています。米国の戦闘艦艇数は、現在の295隻から2054年には390隻に増加すると予想されています。これらの計画では、原子炉、統合電気推進(IEP)システム、高効率ガスタービンなど、利用可能な最先端の推進技術が求められており、これも市場の成長を後押ししています。

舶用推進エンジン調査の場所

北米(米国およびカナダ)、ラテンアメリカ(ブラジル、メキシコ、アルゼンチン、その他のラテンアメリカ)、ヨーロッパ(英国、ドイツ、フランス、イタリア、スペイン、ハンガリー、ベルギー、オランダおよびルクセンブルグ、NORDIC(フィンランド、スウェーデン、ノルウェー) 、デンマーク)、アイルランド、スイス、オーストリア、ポーランド、トルコ、ロシア、その他のヨーロッパ)、ポーランド、トルコ、ロシア、その他のヨーロッパ)、アジア太平洋(中国、インド、日本、韓国、シンガポール、インドネシア、マレーシア) 、オーストラリア、ニュージーランド、その他のアジア太平洋地域)、中東およびアフリカ(イスラエル、GCC(サウジアラビア、UAE、バーレーン、クウェート、カタール、オマーン)、北アフリカ、南アフリカ、その他の中東およびアフリカ

競争力ランドスケープ

SDKI Analyticsの調査者によると、舶用推進エンジンの市場見通しは、大規模企業と中小規模企業といった様々な規模の企業間の市場競争により、細分化されています。調査レポートでは、市場プレーヤーは、製品と技術の投入、戦略的パートナーシップ、協業、買収、事業拡大など、あらゆる機会を捉え、市場全体における競争優位性を獲得しようとしていると指摘されています。

舶用推進エンジン市場で事業を展開している世界有数の企業はどこですか?

弊社の調査レポートによると、世界の舶用推進エンジン市場の成長に重要な役割を果たしている主な主要企業には、Caterpillar Inc.、Wärtsilä Corporation、Rolls-Royce plc、ABB Ltd.、GE Vernovaなどが含まれます。

舶用推進エンジン市場で競合している日本の主要企業はどこですか?

市場展望によると、日本の舶用推進エンジン市場における上位5社は、Mitsubishi Heavy Industries, Ltd.、 Kawasaki Heavy Industries, Ltd.、Yanmar Power Technology Co., Ltd.、Niigata Power Systems Co., Ltd.、IHI Corporationです。

市場調査レポート研究には、世界的な舶用推進エンジン市場分析調査レポートにおける主要企業の詳細な競合分析、企業プロファイル、最近の傾向、主要な市場戦略が含まれています。

舶用推進エンジン市場における最新のニュースや開発は何ですか?

- 2025年11月:YANMAR Marine Internationalは、METSTRADEにおいて、同社が誇る最先端の統合型船舶制御ソリューション「VC30 Vessel Control System(船舶制御システム)」を発表しました。スロットル、ドッキング、エンジンデータ、ジョイスティック操作を1つのプラットフォームに統合し、高輝度4.3インチディスプレイ、部品点数削減によるシンプルな設置、幅広いエンジン互換性を特徴としています。

- 2025年10月:Tsuneishi Shipbuildingは、日本初の水素燃料タグボート「TEN-OH(テンオー)」を竣工しました。12気筒ツインエンジンと高圧水素貯蔵機能を備えた高出力水素内燃機関を搭載しています。日本財団のゼロエミッションシッププロジェクトの一環として開発された本船は、従来型タグボートと比較してCO₂排出量を削減し、脱炭素化された海上運航に貢献します。

舶用推進エンジン主な主要プレーヤー

主要な市場プレーヤーの分析

日本市場のトップ 5 プレーヤー

目次

舶用推進エンジンマーケットレポート

関連レポート

よくある質問

- 2020ー2024年

- 2026-2035年

- 必要に応じて日本語レポートが入手可能

品質と信頼の証