- 2020ー2024年

- 2024-2036年

- 必要に応じて日本語レポートが入手可能

品質と信頼の証

摩擦材市場規模

摩擦材市場の収益は、2023 年に約 223億米ドルに達しました。さらに、当社の摩擦材市場に関する洞察によると、市場は予測期間中に約 5.93% の CAGR で成長し、2036 年までに約 445億米ドルの価値に達すると予想されています。

摩擦材市場分析

市場の定義

表面間に摩擦を生み出し、さまざまな部品の前後の動きを制御できる物質は、摩擦材と呼ばれます。有機材料、無機材料を使用した摩擦材の製造が可能です。摩擦材の製造に最も一般的に使用される材料には、金属、セラミックス、樹脂、繊維などがあります。

摩擦材市場の成長要因

以下は、摩擦材市場の主な成長要因の一部です。

- 航空宇宙製造部門の驚異的な成長– 航空機の需要は商業用途や軍事アプリケーションで、今後で増加すると予想されます。航空旅行の乗客数の増加、エネルギー効率の高い軽飛行機の需要、商業空域の開発、多額の軍事支出はすべて、製造される航空機の数の増加、そして最終的には市場の成長に貢献するはずです。

- 2021―2040 年間に 13,000 機以上になると単通路航空機が納入されると推定されています。さらに、2021 年 6 月― 2022 年 6 月の間に、世界中で運用されている航空機の保有台数が約 12% 増加することが観察されました。

- 貨物列車の数の著しい増加–貨物列車の需要を促進する主な要因の 1 つは、各国間の国境を越えた貿易の増加です。さらに、液体バルク貨物やコンテナ化されていない貨物をある場所から別の場所に運ぶには、鉄道輸送が最も適しています。

- 2021年には2020年と比較して8.7%という顕著な増加を記録しました。

最新の開発

- 2022 年 4 月に、Tenneco は、非アスベスト・オーガニック (NAO) と低鋼 (LS) の利点を組み合わせたハイブリッド摩擦材複合材料の導入を発表しました。

- 2023年4月に、Nippon Steel Corporationは、東海旅客鉄道(株)と共同開発した新幹線用ブレーキパッドが「2020年Minister of Education、Culture、 Sports、 Science、および Technology Award」を受賞したと発表しました。

課題

パンデミックによる2020年の自動車、旅客列車、航空機の製造の一時停止により、予測期間中に市場の成長が大幅に遅れたと考えられます。これらの車両のブレーキシステムなどには摩擦材が使用されており、製造活動の中断により需要が減少しました。

サンプル納品物ショーケース

- 調査競合他社と業界リーダー

- 過去のデータに基づく予測

- 会社の収益シェアモデル

- 地域市場分析

- 市場傾向分析

摩擦材市場レポートの洞察

|

レポートの洞察 |

|

|

CAGR |

5.93% |

|

予測年 |

2024―2036年 |

|

基準年 |

2023年 |

|

予測年の市場価値 |

445億米ドル |

摩擦材市場セグメント

当社は、摩擦材市場に関連するさまざまなセグメントにおける需要と機会を説明する調査を実施しました。当社はタイプ、材料、アプリケーション、エンドユーザー産業、ビジネスタイプに基づいて市場を分割しました。

タイプに基づいて、摩擦材市場は、ディスク、パッド、ブロック、ライニング、その他のタイプに分割されています。これらのうち、パッドのサブセグメントは、車両の動きを遅くし、駐車時に車両を静止状態に保つ重要性があるため、予測期間中に最大の市場シェアを約 33% 保持すると予想されます。

ブレーキパッドにおける環境に優しい摩擦材の需要は、このサブセグメントの成長に大きく貢献すると予想されます。摩擦材の需要を生み出すもう一つの要因は、電気自動車への油圧ブレーキの搭載です。さらに、焼結金属の摩擦材は、長寿命、耐フェード性の向上などの理由から、全地形対応車(ATV)や選別搬送車(STV)に使用されています。

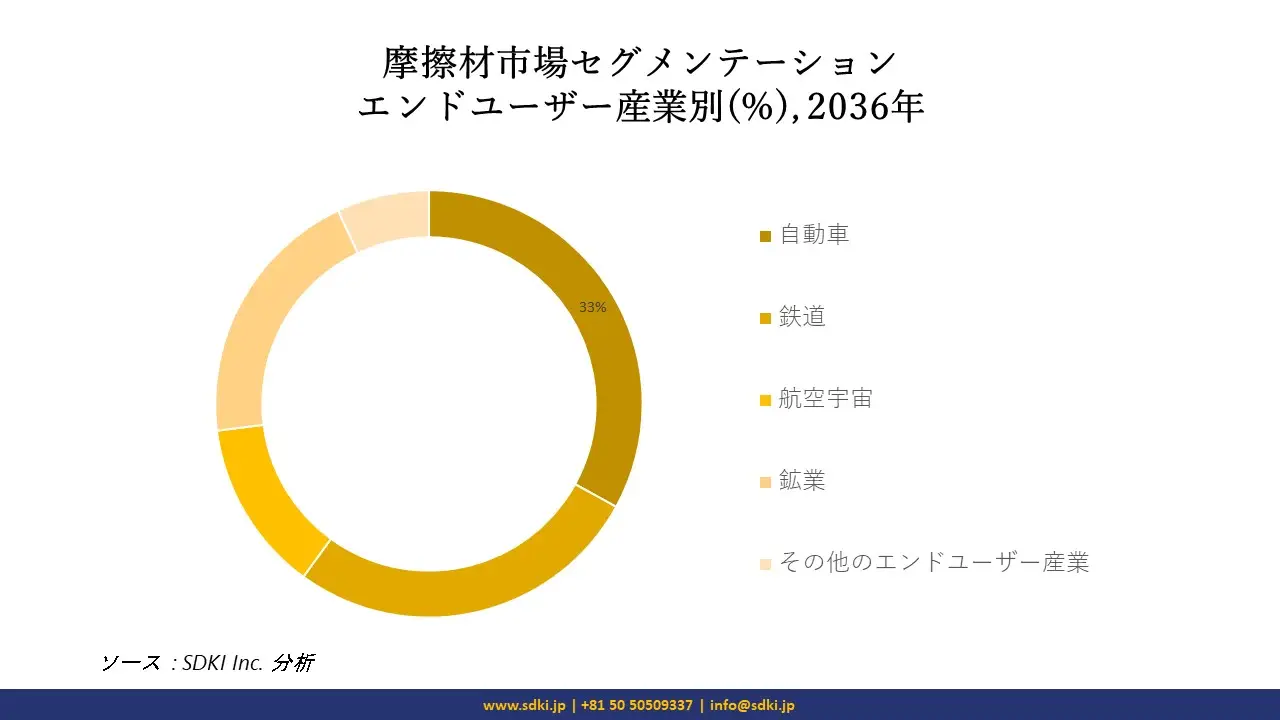

エンドユーザー産業に基づいて、摩擦材市場は、自動車、鉄道、航空宇宙、鉱業、その他のエンドユーザー産業に分割されています。このうち、摩擦材の需要は自動車分野で最も高いと予想されます。自動車分野は、2036 年末までに最大 33% の市場シェアを保持すると予想されています。この分野における摩擦材の主なアプリケーションは、ディスク ブレーキのブレーキ パッドとドラム ブレーキのブレーキ ライニングです。

また、セラミック製の摩擦材は、レース用車両のクラッチシステムにも有用であると考えられている。このようなクラッチシステムは、550℃までの温度でもフェードしません。

|

タイプ別 |

|

|

材料別 |

|

|

アプリケーション別 |

|

|

エンドユーザー産業別 |

|

|

ビジネスタイプ別 |

|

摩擦材市場の地域概要

アジア太平洋地域は摩擦材の最大の地域市場となり、2024―2036 年間に市場シェアは最大 34% になると予想されています。地域市場は、主に産業の成長と大幅な自動車および建設セクターの存在により成長すると予想されます。インドや中国などの国々では、電車、トラック、バス、産業用ロボット、その他の機械に対する幅広い需要があり、これが市場の成長に寄与するはずです。

たとえば、2021 年に中国だけで生産された産業用ロボットの数は 362,999 台以上になると推定されています。さらに、これらの国における電気自動車の需要の増加も市場の成長に大きく寄与するはずです。

日本では、トラックの運行台数の増加により、今後数年間で摩擦材の需要が増加すると予想されています。 2022 年 3 月の時点で、国内で使用のために登録されているトラックは 15百万台以上あると推定されています。

|

北米 |

|

|

ヨーロッパ |

|

|

アジア太平洋地域 |

|

|

ラテンアメリカ |

|

|

中東とアフリカ |

|

北米は、2036 年末までに市場収益の大きなシェアを握ると予想されるもう 1 つの地域です。この地域は、2024―2036 年間に世界市場の最大 34% のシェアを握ると予想されます。地域市場の成長は、主に多くの主要な摩擦材メーカーの存在によって推進されるはずです。さらに、自動車分野からの需要の増加も自動車分野の成長につながるはずです。

この地域では、可処分所得の増加と都市化の進行により、自家用車の需要が増加しています。電子商取引の分野でも目覚ましい進歩があり、トラックの需要が増加しています。国勢調査局によると、2023 年の第 1 四半期から第 2 四半期にかけて、米国における小売電子商取引の売上高は 6.6% 増加しました。

摩擦材調査の場所

北米(米国およびカナダ)、ラテンアメリカ(ブラジル、メキシコ、アルゼンチン、その他のラテンアメリカ)、ヨーロッパ(英国、ドイツ、フランス、イタリア、スペイン、ハンガリー、ベルギー、オランダおよびルクセンブルグ、NORDIC(フィンランド、スウェーデン、ノルウェー) 、デンマーク)、アイルランド、スイス、オーストリア、ポーランド、トルコ、ロシア、その他のヨーロッパ)、ポーランド、トルコ、ロシア、その他のヨーロッパ)、アジア太平洋(中国、インド、日本、韓国、シンガポール、インドネシア、マレーシア) 、オーストラリア、ニュージーランド、その他のアジア太平洋地域)、中東およびアフリカ(イスラエル、GCC(サウジアラビア、UAE、バーレーン、クウェート、カタール、オマーン)、北アフリカ、南アフリカ、その他の中東およびアフリカ

競争力ランドスケープ

世界の摩擦材市場中に主なプレーヤーには、ABS Friction Inc.、Brembo S.p.A.、Miba AG、Tenneco Inc.、Carlisle Brake & Friction、などが含まれます。さらに、日本市場のトップ 5 プレーヤーは、Akebono Brake Industry Co., Ltd.、AISIN CORPORATION、Nisshinbo Holdings Inc.、NSK Warner Co., Ltd.、および Resonac Holdings Co., Ltd.、 などです。この調査には、世界の摩擦材市場におけるこれらの主要なプレーヤーの詳細な競争分析、企業概要、最近の傾向、および主要な市場戦略が含まれています。

摩擦材主な主要プレーヤー

主要な市場プレーヤーの分析

日本市場のトップ 5 プレーヤー

目次

摩擦材マーケットレポート

関連レポート

- 2020ー2024年

- 2024-2036年

- 必要に応じて日本語レポートが入手可能

品質と信頼の証