- 2020ー2024年

- 2026-2035年

- 必要に応じて日本語レポートが入手可能

品質と信頼の証

半導体ウエハー研磨・研削装置市場規模

2026―2035年の半導体ウエハー研磨・研削装置市場の市場規模はどのくらいですか?

半導体ウエハー研磨・研削装置市場に関する当社の調査レポートによると、同市場は予測期間(2026―2035年)の間に複利年間成長率(CAGR)4.8%で成長すると予想されています。将来的には、市場規模は68億米ドルに達する見込みです。しかし、当社の調査アナリストによると、基準年の市場規模は31億米ドルでしました。

半導体ウエハー研磨・研削装置市場において、市場シェアの面でどの地域が優位を占めると予想されますか?

半導体ウエハー研磨・研削装置に関する当社の市場調査によると、アジア太平洋地域の市場は予測期間中に約63%という圧倒的な市場シェアを維持し、複利年間成長率(CAGR)5.4%という最高成長率で拡大すると予想されます。これは今後数年間、有望な成長機会をもたらすでしょう。この成長は主に、主要なファブエコシステムと設備投資、半導体デバイスの複雑化、そしてロジック、メモリ、SiC/GaNアプリケーションにおける超平坦で欠陥のないウェーハへのニーズの高まりが、高精度研磨・研削ツールへの投資を促進していることに起因します。

半導体ウエハー研磨・研削装置市場分析

半導体ウエハー研磨・研削装置とは何ですか?

半導体ウエハー研磨・研削装置とは、チップ製造工程において半導体ウェーハを平滑化、薄化、及び加工するために使用される機械を指します。研削装置は、余分な材料を除去して必要なウェーハ厚さを実現するのに役立ちます。化学機械研磨(CMP)と呼ばれる研磨装置は、平坦で欠陥のない表面を作り出すのに役立ちます。

半導体ウエハー研磨・研削装置市場における最近の傾向は何ですか?

当社の半導体ウエハー研磨・研削装置市場分析調査レポートによると、以下の市場傾向と要因が市場成長の主要な推進力として貢献すると予測されています。

- 高精度かつ高度なウェーハ処理の需要 –

半導体ウエハー研磨・研削装置市場は、特に先端ノード製造において、チップメーカーが極めて高精度なウェーハ表面を必要とするため拡大しています。当社の調査レポートによると、これにより市場全体の見通しが向上しています。研磨・研削ツールは、高性能ロジック、メモリ、パワーデバイスに必要な、超平坦で欠陥のないウェーハを実現するために不可欠です。

米国会計検査院(GAO)によると、最近採択された半導体プロジェクトは、材料からパッケージングに至るまでのサプライチェーンのギャップ解消に重点を置いており、これらのプロジェクトの約40%は最先端のロジックチップの製造を目的としています。こうした傾向が、高精度ウェハ処理装置の需要を押し上げています。

- 政府支援が製造及び設備需要を押し上げる –

半導体ウエハー研磨・研削装置市場のもう一つの重要な推進要因は、半導体製造工場の拡張に対する政府の強力な支援です。これは、当社の調査レポートで強調されているように、市場の見通しを改善します。CHIPSや科学法などのプログラムに基づく公的資金は、企業がウェーハ製造施設を建設・拡張することを奨励します。

米国商務省の報告書によると、CHIPS法は半導体製造を支援するため、ウェハー製造工場や関連機器を含め、約390億米ドルの製造奨励金を認可しています。この資金は、研磨機や研削機といった精密なウェハー加工装置への投資を促進します。

半導体ウエハー研磨・研削装置市場は、日本の市場参入企業にどのようなメリットをもたらしますか?

日本では、半導体ウエハー研磨・研削装置市場が国内メーカーを支えています。この市場は、国内メーカーがグローバルなチップサプライチェーンで競争力を維持する上で役立っています。日本は依然として一部の半導体製造装置を輸入に依存しており、これは国内サプライヤーにとって課題となっています。同時に、国内イノベーションの余地も生み出しています。

政府貿易省の報告書によると、2024年には日本の半導体製造装置メーカーがシングルウェハ洗浄装置の世界市場の60―80%を占める見込みであります。これは高精度装置に対する需要の高まりを反映しています。日本国内での半導体生産拡大に伴い、市場の見通しは明るくなっています。官民連携事業も新たな半導体工場の建設を後押ししています。

日本政府は、資金援助や補助金を通じてこの成長を支援しています。これらの政策は、研究開発、設備開発、サプライチェーンの強靭化に重点を置いています。ラピダス関連プロジェクトを含む先進製造エコシステムへの支援は、設備メーカーに直接的な利益をもたらす。最近の調査報告書では、高精度ウェハ研磨・研削工具への強い関心が成長を後押ししていることが証明されました。

半導体ウエハー研磨・研削装置市場に影響を与える主な制約要因は何ですか?

半導体ウエハー研磨・研削装置市場は、特殊消耗品の価格高騰の影響を大きく受けています。具体的には、研磨パッド、スラリー、研削砥石などの初期費用が高額になるため、所有コストが増大し、購入意欲が低下します。これは主に、メーカーが運用コストの増加と投資収益率を天秤にかけて判断していることに起因します。

サンプル納品物ショーケース

- 調査競合他社と業界リーダー

- 過去のデータに基づく予測

- 会社の収益シェアモデル

- 地域市場分析

- 市場傾向分析

半導体ウエハー研磨・研削装置市場レポートの洞察

半導体ウエハー研磨・研削装置市場の将来展望はどうなっていますか?

SDKI Analyticsの専門家によると、半導体ウエハー研磨・研削装置市場の世界シェアに関するレポートの洞察は以下のとおりです。

|

レポートのインサイト |

|

|

2026―2035年の複利年間成長率(CAGR) |

4.8% |

|

2025年の市場価値 |

31億米ドル |

|

2035年の市場価値 |

68億米ドル |

|

過去のデータ共有 |

過去5年間から2024年まで |

|

未来予測完了 |

2035年までの今後10年間 |

|

ページ数 |

200+ページ |

ソース: SDKI Analytics 専門家分析

半導体ウエハー研磨・研削装置市場はどのように区分されていますか?

当社は、半導体ウエハー研磨・研削装置市場の見通しに関連する様々なセグメントにおける需要と機会を説明する調査を実施しました。市場は、機器タイプ別、ウェハーサイズ別、最終処理別、購入者タイプ別セグメントに分割されています。

半導体ウエハー研磨・研削装置市場は、機器タイプ別どのように分割されていますか?

半導体ウエハー研磨・研削装置市場の見通しにおいて、機器タイプ別は重要なセグメントであり、化学機械研磨(CMP)、ウェーハ研削、ラッピング/平面加工が含まれます。化学機械研磨(CMP)は、高度なデバイス製造のための超平坦ウェーハ表面を実現する上で不可欠な役割を担っているため、2035年までに推定50%のシェアを占め、市場を席巻すると予測されています。CMPは、余分な材料を除去し、ナノメートルレベルの表面平坦性を確保するために、半導体製造のフロントエンドで広く使用されています。

半導体工業会(SIA)の2024年版アップデートによると、世界の半導体売上高は2024年に6,276億米ドルに達し、ウェハ処理装置の需要を直接支える持続的な生産量を反映している。チップの複雑化と多層デバイスアーキテクチャの拡大に伴い、精密な平坦化プロセスが引き続き求められています。高性能ロジックデバイス及びメモリデバイスを実現する上でCMPが果たす中心的な役割は、装置タイプ別セグメントにおけるCMPのリーダーシップを確固たるものにしています。

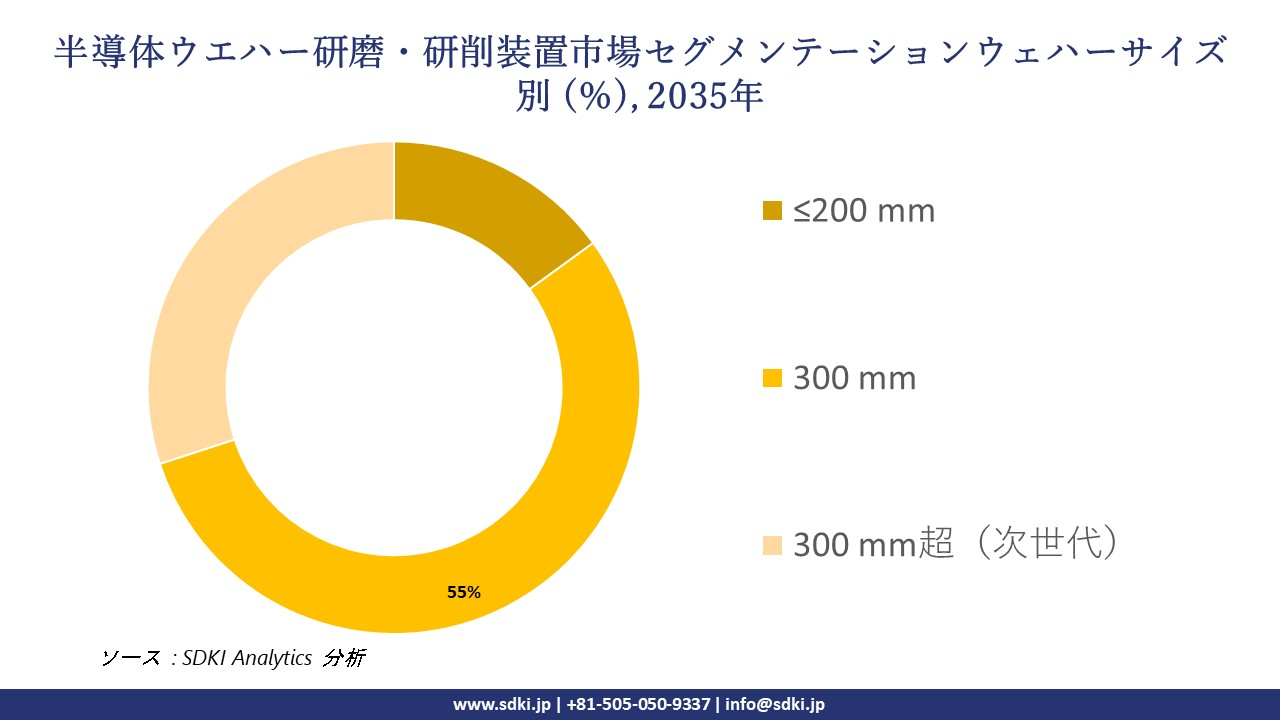

半導体ウエハー研磨・研削装置市場は、ウェハーサイズ別にどのように分割されていますか?

半導体ウエハー研磨・研削装置市場におけるウェハーサイズ別は、≤200 mm、300 mm、300 mm超(次世代)に分類されます。300 mm超(次世代)セグメントは、大規模チップ製造における生産性とコスト効率の高さから、2035年までに推定55%のシェアを占め、市場を牽引すると予想されています。ウェハサイズが大きくなることで、1枚のウェハに集積できるチップ数が増え、製造全体の経済性が向上します。

高度な製造設備が大量生産能力を拡大し続ける中、300 mm超(次世代)はロジック及びメモリ用途における業界標準であり続けています。その運用効率の高さと最新の製造インフラとの互換性により、ウェハサイズ区分において圧倒的な地位を維持しています。

以下に、半導体ウエハー研磨・研削装置市場に適用されるセグメントの一覧を示します。

|

親セグメント |

サブセグメント |

|

機器タイプ別 |

|

|

ウェハーサイズ別 |

|

|

最終処理別 |

|

|

購入者タイプ別 |

|

ソース: SDKI Analytics 専門家分析

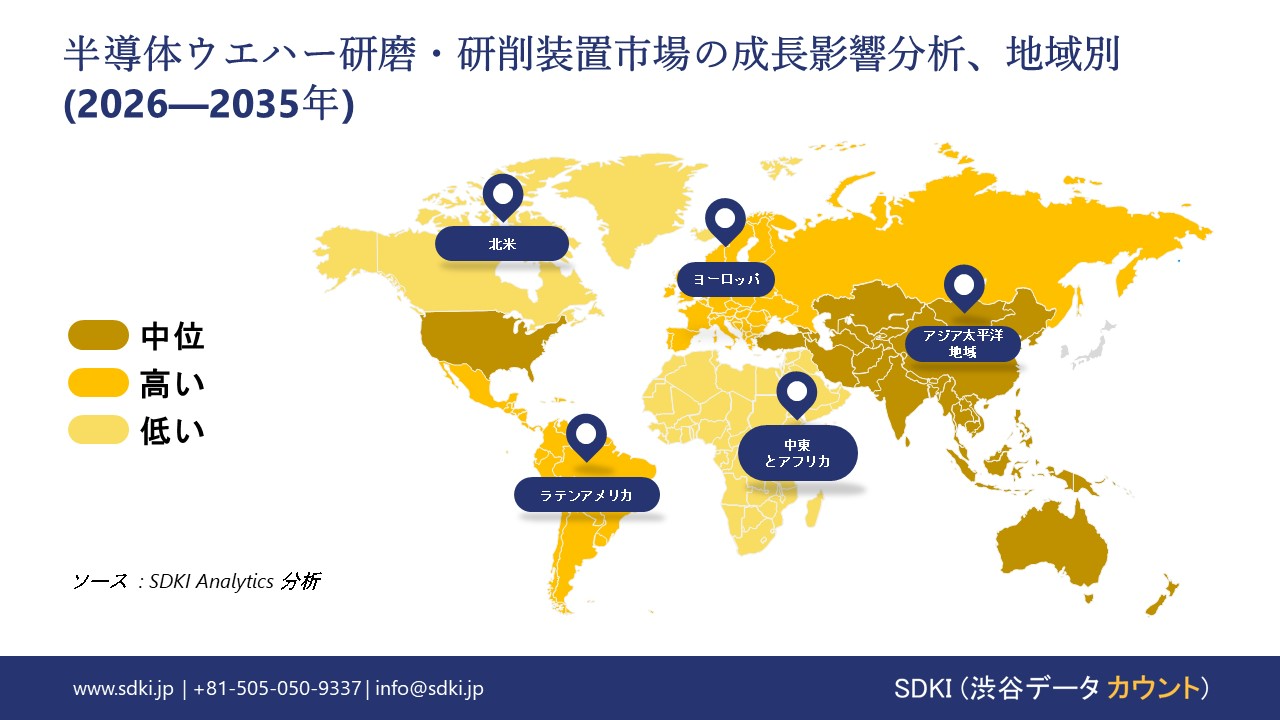

半導体ウエハー研磨・研削装置市場の傾向分析と将来予測:地域別市場概況

アジア太平洋地域は、分析期間終了までに世界の半導体ウエハー研磨・研削装置市場において63%という圧倒的なシェアを占め、市場を牽引する態勢を整えています。同地域は、国内の半導体及び電子機器生産能力と大規模な国際供給網において、そのリーダーシップを確固たるものにしています。

これを裏付けるように、経済複雑性観測所(OEC)によると、2024年には世界最大の供給国及び貿易先は主に中国、マレーシア、日本、香港に集中しており、中でも中国は535億米ドル相当の輸出額で最大を占めました。

SDKI Analyticsの専門家は、半導体ウエハー研磨・研削装置市場に関するこの調査レポートのために、以下の国と地域を調査しました。

|

地域 |

国 |

|

北米 |

|

|

ヨーロッパ |

|

|

アジア太平洋地域 |

|

|

ラテンアメリカ |

|

|

中東及びアフリカ |

|

ソース: SDKI Analytics 専門家分析

北米における半導体ウエハー研磨・研削装置市場の市場実績はどのようなものですか?

北米における半導体ウエハー研磨・研削装置市場は、評価期間を通じて収益性の高い市場であり続けると予想されます。自動車、AI、先端エレクトロニクス産業向けの半導体関連新技術の開発が着実に進展していることから、同地域の市場見通しは大幅な成長を示しています。

こうした動きは、米国政府が半導体生産における自給効率の向上に必死に取り組んでいることによってさらに後押しされています。これは、2022年に施行されたCHIPS・科学法によっても明らかであり、同法は2023年に米国の国内半導体産業を強化するために527億米ドルを計上ました。

半導体ウエハー研磨・研削装置調査の場所

北米(米国およびカナダ)、ラテンアメリカ(ブラジル、メキシコ、アルゼンチン、その他のラテンアメリカ)、ヨーロッパ(英国、ドイツ、フランス、イタリア、スペイン、ハンガリー、ベルギー、オランダおよびルクセンブルグ、NORDIC(フィンランド、スウェーデン、ノルウェー) 、デンマーク)、アイルランド、スイス、オーストリア、ポーランド、トルコ、ロシア、その他のヨーロッパ)、ポーランド、トルコ、ロシア、その他のヨーロッパ)、アジア太平洋(中国、インド、日本、韓国、シンガポール、インドネシア、マレーシア) 、オーストラリア、ニュージーランド、その他のアジア太平洋地域)、中東およびアフリカ(イスラエル、GCC(サウジアラビア、UAE、バーレーン、クウェート、カタール、オマーン)、北アフリカ、南アフリカ、その他の中東およびアフリカ

競争力ランドスケープ

SDKI Analyticsの調査員によると、半導体ウエハー研磨・研削装置の市場見通しは、大企業と中小企業といった規模の異なる企業間の競争により、分割されています。調査報告書によると、市場参加者は、製品や技術の発表、戦略的提携、協力、買収、事業拡大など、あらゆる機会を活用して、市場全体の見通しにおいて競争優位性を獲得しようとしています。

半導体ウエハー研磨・研削装置市場において、世界をリードする企業はどこですか?

当社の調査レポートによると、世界の半導体ウエハー研磨・研削装置市場の成長において重要な役割を担う主要企業には、 Applied Materials Inc.、Revasum Inc.、Lam Research Corp.、Logitech Ltd.、SKC Co., Ltd.などが含まれます。

半導体ウエハー研磨・研削装置市場で競合する主要な日本企業はどこですか?

市場見通しによると、日本の半導体ウエハー研磨・研削装置市場の上位5社は、DISCO Corporation、 Tokyo Seimitsu (ACCRETECH)、 Ebara Corporation、 Fujimi Incorporated、 AGC Inc.などであります。

この市場調査レポートには、世界の半導体ウエハー研磨・研削装置市場分析調査レポートにおける主要企業の詳細な競合分析、企業プロファイル、最近の傾向、及び主要な市場戦略が含まれています。

半導体ウエハー研磨・研削装置市場における最新のニュースや傾向は何ですか?

- 2026年2月 – Lam Research Corporationは、米国における半導体製造の成長支援を強化し、マイクロン社との連携を深め、先進的なメモリチップの生産とイノベーションを加速させるため、アイダホ州ボイシに新たなオフィスを開設しました。

- 2025年12月 – EBARAは、SEMICON Japan 2025にゴールドスポンサーとして出展し、CMP、めっきシステム、真空ポンプなどを展示するとともに、CMP後の洗浄傾向や関連イベントに関するセミナーを開催することを発表しました。

半導体ウエハー研磨・研削装置主な主要プレーヤー

主要な市場プレーヤーの分析

日本市場のトップ 5 プレーヤー

目次

半導体ウエハー研磨・研削装置マーケットレポート

関連レポート

よくある質問

- 2020ー2024年

- 2026-2035年

- 必要に応じて日本語レポートが入手可能

品質と信頼の証