ベクトル制御市場調査レポート、規模とシェア、成長機会、及び傾向洞察分析 ― 製品タイプ別、ベクトル型別、アプリケーション別、分布別、地域別―世界市場の見通しと予測 2026-2035年

出版日: Mar 2026

- 2020ー2024年

- 2026-2035年

- 必要に応じて日本語レポートが入手可能

品質と信頼の証

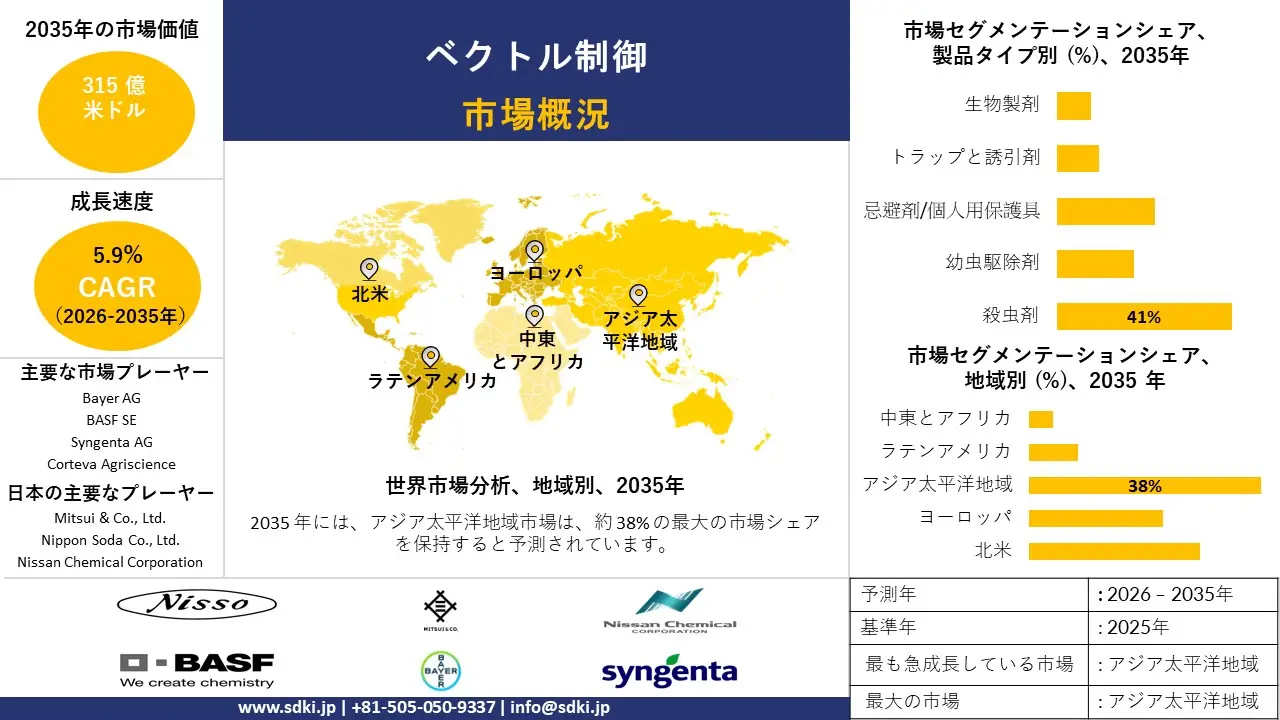

ベクトル制御市場規模

2026―2035年のベクトル制御市場の規模はどれくらいですか?

ベクトル制御市場に関する私たちの調査レポートによると、市場は予測期間(2026―2035年)の間に約5.9%の複利年間成長率(CAGR)で成長すると予想されています。2035年には、世界市場は約315億米ドルに達すると予想されています。しかし、私たちの調査アナリストによると、基準年である2025年の市場規模は約175億米ドルとされています。

市場シェアの観点から、ベクトル制御市場を支配すると予想される地域はどれですか?

ベクトル制御に関する私たちの市場調査によると、アジア太平洋地域は約38%という圧倒的な市場シェアを維持し、予測期間中に最も高いCAGRを示すと予測されており、世界市場における同地域の極めて重要な役割を浮き彫りにしています。この二重の優位性は、媒介生物媒介性疾患の蔓延、急速な都市化、政府による公衆衛生への支援策、人口密度の高い国における総合的病害虫管理プログラムへの多額の投資など、地域特有の成長要因によって支えられています。

ベクトル制御市場分析

ベクトル制御とは何ですか?

ベクトル制御市場は、蚊、ダニ、げっ歯類などの病原体を媒介する害虫を管理・駆除するための製品、サービス、及び戦略で構成されています。これには、マラリア、デング熱、ジカウイルスなどの病気の蔓延を防ぐことを目的とした化学殺虫剤、生物兵器、トラップ、環境管理ソリューションが含まれます。

ベクトル制御市場の最近の傾向は何ですか?

私たちのベクトル制御市場分析調査レポートによると、以下の市場傾向と要因が市場成長の中核的な原動力として貢献すると予測されています。

- 世界公衆衛生戦略は媒介動物対策能力の強化を義務付けている –

私たちの調査報告書によると、WHOが承認した世界戦略は、媒介動物対策を公衆衛生上の恒久的な優先事項として制度化しています。「世界媒介動物対策対応2017-2030」は、加盟国が採択したWHO承認の戦略であり、媒介動物監視の拡大、人的資源能力の強化、そして世界規模での総合的な媒介動物対策の改善を求めています。GVCRは、2030年までの国家計画のための戦略的枠組みを明確に定めています。 量的に言えば、GVCR の柱は、感染症の 17% 以上を占め、毎年 700000人以上の死因となっている媒介生物媒介性疾患の負担を軽減することを目指しています。 質的に言えば、この戦略は政府に監視システムと介入ツールの強化を約束し、ベクトル制御製品とサービスの長期的需要を拡大しています。

-

媒介性疾患の持続的な高負担が政策主導の需要を支えている –

私たちの調査報告書によると、未解決の世界的な疾病蔓延は、媒介性疾患対策への非裁量的な需要を促しています。WHOのサーベイランスデータによると、媒介性疾患は世界的な健康問題として依然として大きな負担となっており、毎年数億人がマラリアとデング熱に罹患し、熱帯、亜熱帯、温帯地域にまたがる感染リスクにさらされています。この疫学的圧力により、各国政府は殺虫剤処理済みの蚊帳、屋内残留散布、幼虫管理といった媒介性疾患対策プログラムを維持・拡大する義務を負っています。疾病の撲滅が不完全なため、媒介性疾患対策の需要は循環的というよりはむしろ防衛的なものとなり、公衆衛生上の必要性に突き動かされる一貫した市場活動を支えています。

ベクトル制御市場は日本の市場プレーヤーにどのような利益をもたらすですか?

ベクトル制御市場は、バリューチェーン全体にわたって日本の市場プレーヤーに多くの機会を提供しています。日本国内の機会は、政府主導の感染症対策に基づいています。例えば、内閣府の感染症危機管理基本計画では、蚊媒介性感染症対策を国土強靱化計画の重点分野として位置付けており、安定したB2G需要を強化しています。さらに、経済産業省の化学産業ビジョンでは、害虫防除用薬剤は、継続的な研究開発支援により輸出可能な特殊製品として言及されており、2030年までの市場見通しは良好です。企業側では、住友化学は2024年度有価証券報告書において、ベクトル制御用殺虫剤と公衆衛生ソリューションの継続的なグローバル展開を開示し、海外の疾病流行地域を重点市場と位置付けています。さらに、アース製薬は2024年度アニュアルレポートで、家庭用及び業務用害虫防除製品の国際的な成長について言及しており、これは国内のイノベーションと輸出収益化を一致させています。 WHO関連の管理プログラムへの日本の参加や、JETROが記録した公衆衛生輸出は、サプライチェーンへの参加を支えています。政府の化学メーカー調査によると、2024年には海外の景況感が改善し、堅調な輸出機会が強化されています。

ベクトル制御市場に影響を与える主な制約は何ですか?

ベクトル制御市場における主要な制約要因の一つは、主要な病原体を媒介する蚊やその他の害虫における殺虫剤耐性の増大です。これにより、既存の化学防除方法の有効性が低下し、新たな解決策や総合的な管理戦略の開発に多額の費用がかかります。

サンプル納品物ショーケース

- 調査競合他社と業界リーダー

- 過去のデータに基づく予測

- 会社の収益シェアモデル

- 地域市場分析

- 市場傾向分析

ベクトル制御市場レポートの洞察

ベクトル制御市場の今後の見通しはどのようなものですか?

SDKI Analyticsの専門家によると、ベクトル制御市場の世界シェアに関連するレポートの洞察は以下の通りです。

|

レポートの洞察 |

|

|

2026―2035年のCAGR |

5.9% |

|

2025年の市場価値 |

175億米ドル |

|

2035年の市場価値 |

315億米ドル |

|

履歴データの共有 |

過去5年間 2024年まで |

|

未来予測は完了 |

2035年までの今後10年間 |

|

ページ数 |

200+ページ |

ソース: SDKI Analytics 専門家分析

ベクトル制御市場はどのようにセグメントに分割されていますか?

ベクトル制御市場の展望に関連する様々なセグメントにおける需要と機会を説明する調査を実施しました。市場は、製品タイプ別、ベクトル型別、アプリケーション別、分布別にセグメントに分割されています。

ベクトル制御市場は製品タイプ別どのように分割されていますか?

製品タイプ別に基づいて、ベクトル制御市場は、殺虫剤、幼虫駆除剤、忌避剤/個人用保護具、トラップと誘引剤、生物製剤に分割されます。調査報告書によると、蚊などの成虫媒介生物の防除における広範な使用を反映し、殺虫剤は2035年までに市場の41%を占めると予想されています。殺虫剤は、媒介生物‑媒介性疾患の伝播を減らすための公衆衛生戦略において依然として中心的な役割を果たしています。世界保健機関(WHO)によると、世界の3百万人以上の人々が、殺虫剤、幼虫駆除剤、忌避剤または個人用保護製品、捕獲器及び誘引剤、生物製剤を使用しています。 マラリア流行国には、これまでに数十億枚の殺虫剤‑処理済み蚊帳(ITN)が配布されており、ベクトル制御は世界で最も大規模な予防介入の一つとなっています。これらの処理済み蚊帳と屋内残留散布プログラムは、蚊との接触と病気の蔓延を減らすために殺虫剤製品に依存しています。この大規模な展開は、特にマラリアとデング熱が依然として大きな健康被害をもたらしている地域において、殺虫剤市場の明るい見通しを裏付けています。殺虫剤はまた、幼虫駆除剤や個人用防除忌避剤などの他のツールを補完し、公衆衛生枠組みの下での総合的な防除戦略を形成します。

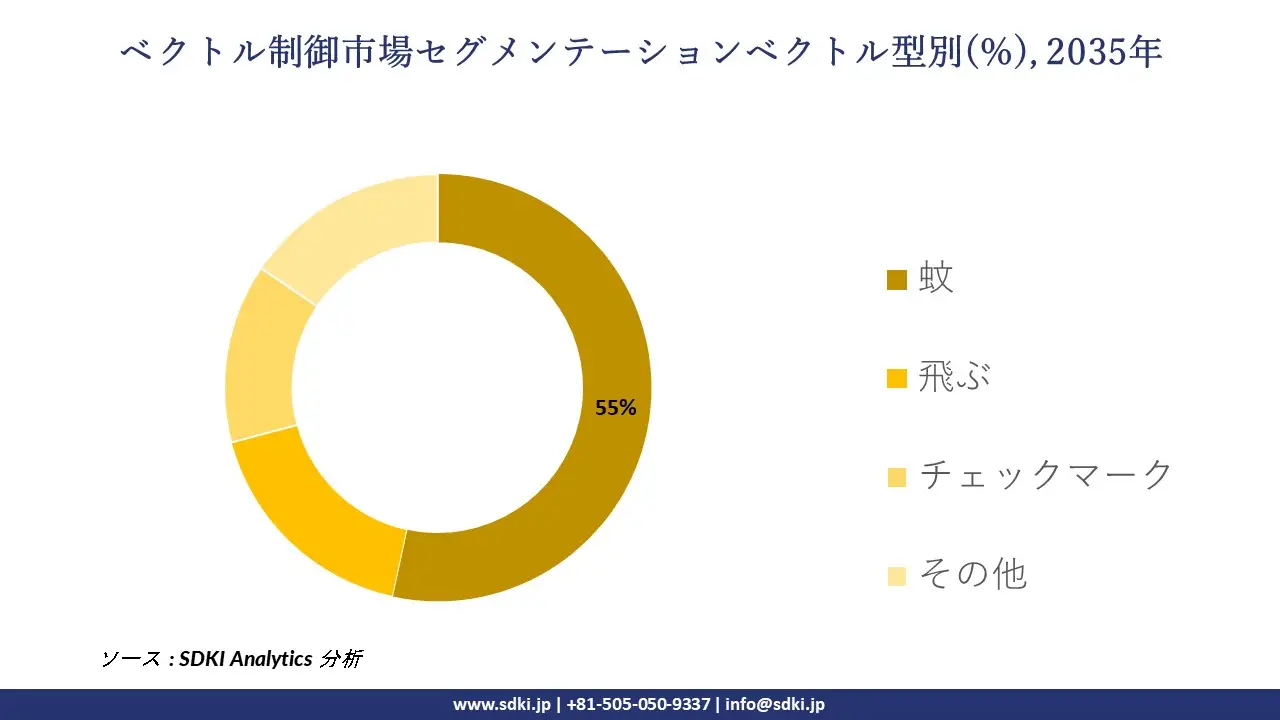

ベクトル制御市場はベクトル型別どのように分割されていますか?

ベクトル型別に基づいて、ベクトル制御市場は蚊、飛ぶ、チェックマーク、その他に分割されます。調査報告書によると、 蚊は2035年までに52%と最大のシェアを占めると予測されています。‑Malaria, Dengue Fever, Zika Feverなど、蚊媒介性疾患が世界的に蔓延しているため、蚊の駆除は依然として最も重要な分野です。蚊の個体数密度と疾患の伝染率の高さは、特殊な防除製品の需要を高めています。蚊の駆除には、殺虫網、噴霧、幼虫駆除、生息地管理などが含まれます。これらのツールは、住宅、商業施設、農業施設における疾患発生率の低減と公衆衛生の保護に不可欠です。世界中で疾患の蔓延制約に向けた取り組みが強化されているため、蚊媒介性疾患の駆除市場の見通しは依然として良好です。

以下は、ベクトル制御市場に該当するセグメントのリストです。

|

親セグメント |

サブ‑セグメント |

|

製品タイプ別 |

|

|

ベクトル型別 |

|

|

アプリケーション別 |

|

|

分布別 |

|

ソース: SDKI Analytics 専門家分析

ベクトル制御市場傾向分析と将来予測:地域市場展望概要

アジア太平洋地域におけるデング熱、マラリア、日本脳炎といった媒介性疾患の蔓延は、大規模な対策を必要としています。インドなどの国では、国立媒介性疾患対策センター(NCVBDC)が2024年に23,3519件以上のデング熱症例と297件の死亡を報告しました。公表されているサーベイランスデータは、媒介性疾患対策への継続的かつ緊急的な公的支出を正当化しています。その結果、各国政府は国家対策プログラムに特定の予算を割り当て、調達に直接資金を提供しています。国家保健ミッションは、NCVBDCに対し、この地域における媒介性疾患対策のために多額の資金を割り当てており、これは媒介性疾患対策の大きな成長要因となっています。

SDKI Analyticsの専門家は、ベクトル制御市場に関するこの調査レポートのために、以下の国と地域を調査しました。

|

地域 |

国 |

|

北米 |

|

|

ヨーロッパ |

|

|

アジア太平洋地域 |

|

|

ラテンアメリカ |

|

|

中東及びアフリカ |

|

ソース: SDKI Analytics 専門家分析

北米におけるベクトル制御市場のパフォーマンスはどうですか?

北米では、連邦政府と州政府による公衆衛生上の緊急事態への備えのための資金提供が、各国における媒介蚊の駆除を推進しています。連邦政府と州政府の公衆衛生機関は、病原体を媒介する蚊の生息範囲の拡大を追跡し、地域的な駆除プログラムを推進しています。CDCの報告によると、2024年のデング熱の症例数は、米国、カナダ、メキシコなどを含むアメリカ大陸全体で約13百万人に達すると予想されています。2023年には、米国ではフロリダ州とテキサス州で20年ぶりにマラリアの地域感染例が、カリフォルニア州とアリゾナ州でもデング熱の地域感染例が記録されました。これは公衆衛生への脅威を示しており、この地域における媒介蚊駆除の必要性を浮き彫りにしています。

ベクトル制御調査の場所

北米(米国およびカナダ)、ラテンアメリカ(ブラジル、メキシコ、アルゼンチン、その他のラテンアメリカ)、ヨーロッパ(英国、ドイツ、フランス、イタリア、スペイン、ハンガリー、ベルギー、オランダおよびルクセンブルグ、NORDIC(フィンランド、スウェーデン、ノルウェー) 、デンマーク)、アイルランド、スイス、オーストリア、ポーランド、トルコ、ロシア、その他のヨーロッパ)、ポーランド、トルコ、ロシア、その他のヨーロッパ)、アジア太平洋(中国、インド、日本、韓国、シンガポール、インドネシア、マレーシア) 、オーストラリア、ニュージーランド、その他のアジア太平洋地域)、中東およびアフリカ(イスラエル、GCC(サウジアラビア、UAE、バーレーン、クウェート、カタール、オマーン)、北アフリカ、南アフリカ、その他の中東およびアフリカ

競争力ランドスケープ

SDKI Analyticsの調査者によると、ベクトル制御市場見通しは、大規模企業と中小規模企業といった様々な規模の企業間の市場競争により、分割されています。調査レポートでは、市場プレーヤーは、製品や技術の投入、戦略的パートナーシップ、協業、買収、事業拡大など、あらゆる機会を捉え、市場全体における競争優位性を獲得しようとしていると指摘されています。

ベクトル制御市場で活動している世界有数の企業はどれですか?

私たちの調査レポートによると、世界的なベクトル制御市場の成長に重要な役割を果たしている主な主要企業には、 Bayer AG、 BASF SE、 Syngenta AG、 Corteva Agriscience、 Sumitomo Chemical Co. Ltdなどが含まれます。

ベクトル制御市場で競合している日本の主要企業はどこですか?

市場展望によると、日本のベクトル制御市場のトップ5企業は、Sumitomo Chemical Co.Ltd.、 Mitsui & Co. Ltd.、 Nippon Soda Co. Ltd.、 Nissan Chemical Corporation、 Earth Chemical Co. Ltdなどです。

ベクトル制御市場分析調査レポートにおける主要企業の詳細な競合分析、企業プロファイル、最近の傾向、主要な市場戦略が含まれています。

ベクトル制御市場における最新のニュースや傾向は何ですか?

- 10月 2025年:Oxitec Ltdが世界最大の蚊製造施設を稼働 ブラジルのカンピナスに、ボルバキア‑媒介蚊及びネッタイシマカ媒介蚊対策ソリューションを世界規模で供給する施設を建設する。この施設は、最大 190 毎週数百万匹のボルバキア蚊の卵を生産し、世界中で蚊媒介性疾患と闘う政府や地域社会へのベクトル制御製品の供給を強化します‑。

- 10月 2025年: SORA Technology Co., Ltd.は、東京都の「GlobalXpander Tokyo」プログラムに採択され、‑タンザニアのザンジバル島でAIドローンを用いたマラリアベクトル制御の実証事業を開始します。この取り組みでは、AIによる水域検知とドローンによる幼虫駆除剤散布を活用し、マラリア媒介生物の繁殖地を特定・駆除することで、世界規模のベクトル制御のための拡張可能なモデルを構築します。

ベクトル制御主な主要プレーヤー

主要な市場プレーヤーの分析

日本市場のトップ 5 プレーヤー

目次

ベクトル制御マーケットレポート

関連レポート

よくある質問

- 2020ー2024年

- 2026-2035年

- 必要に応じて日本語レポートが入手可能

品質と信頼の証