- 2020ー2024年

- 2026-2035年

- 必要に応じて日本語レポートが入手可能

品質と信頼の証

先月は251件以上の問い合わせ

出版日: Aug 2026

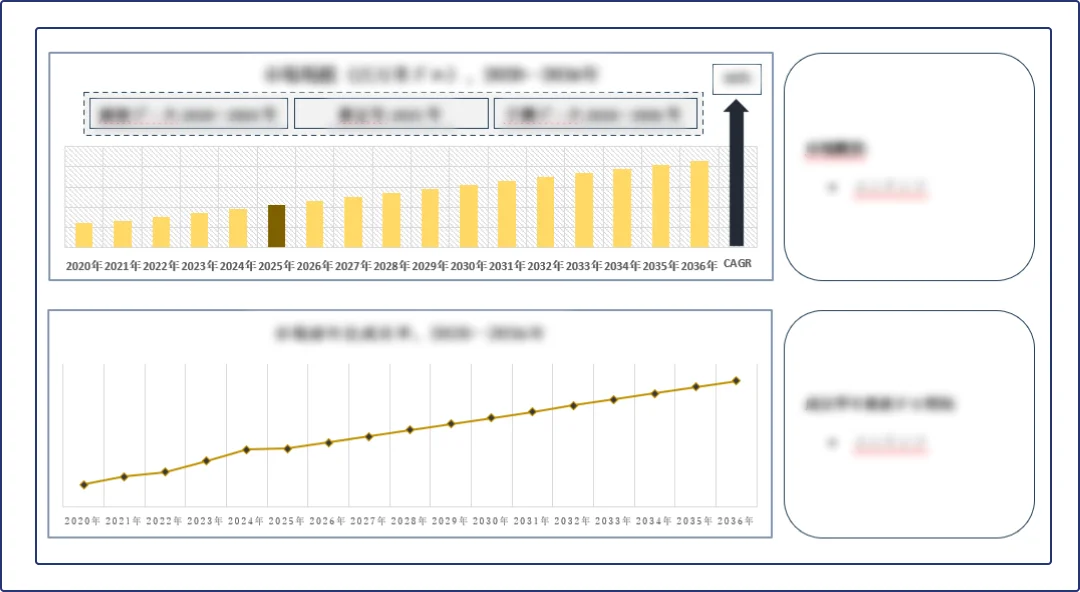

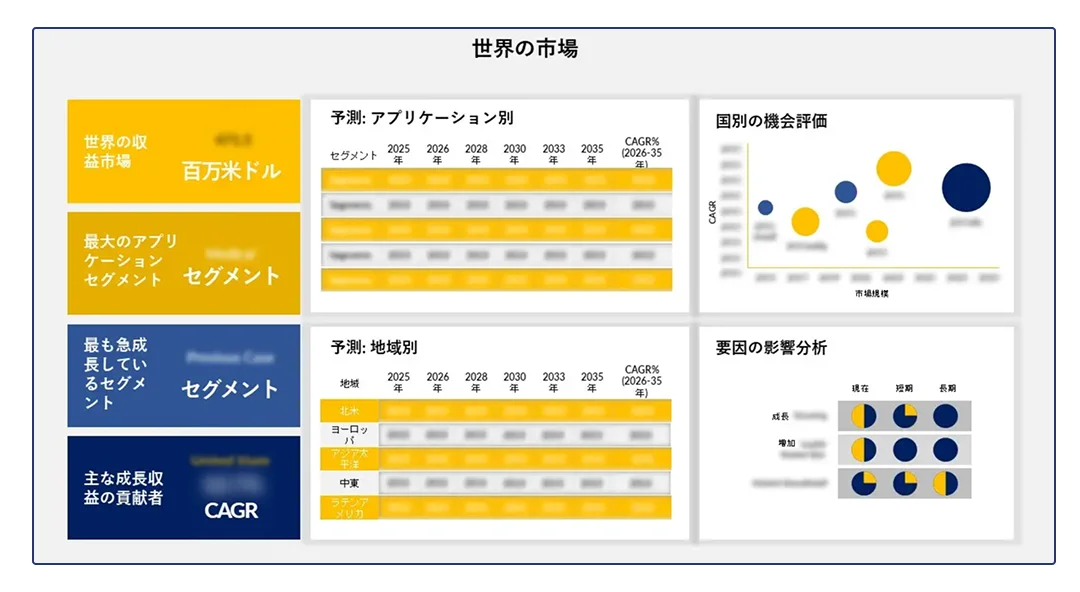

人工膝関節市場の調査レポートによると、SDKI Analyticsのアナリストは次のような結論を出しています:

- 2026-2035 年の CAGR: 7%

- 2035年の予想市場規模: 178億米ドル

- 2025年の市場規模: 91億米ドル

サンプル納品物ショーケース

本レポートに含まれる戦略的情報

当社の包括的な分析は、お客様が最も重要なビジネス上の疑問に答え、データに基づいた自信のある意思決定を行うのに役立ちます。

市場見通しと予測

- 現在の市場規模と2035年までの予測市場規模はどの程度ですか?

- 予測期間中、市場はどの程度の年平均成長率(CAGR)を達成すると見込まれていますか?

- どの市場セグメントが最大の収益を生み出すと予想されていますか?

- どのアプリケーションセグメントが最も急速な成長を遂げると予測されていますか?

- エンドユーザー業界ごとに、市場需要はどのように推移していくと見込まれますか?

- 将来の業界の成長を形作る主な市場トレンドは何ですか?

- 市場拡大に影響を与えているマクロ経済要因は何ですか?

- 主な成長促進要因と市場の制約要因は何ですか?

競合情報および地域情報

- 現在、世界の市場を主導している地域はどこですか?

- どの地域市場が最も急速に成長すると予測されていますか?

- 投資の機会が最も大きい国はどこですか?

- 市場で事業を展開している主要企業はどこですか?

- どのような競争戦略が業界の情勢を形成していますか?

- 最近の合併・買収、提携、あるいは新製品の投入が、競争環境にどのような影響を与えていますか?

- 主要企業間での市場シェアはどのように分布していますか?

- 市場の成長に影響を与えている地域ごとの規制や政策にはどのようなものがありますか?

戦略的ビジネスインサイト

- 2035年までに、最も魅力的な投資機会はどこにあるのか?

- どの新興技術が業界を変革しているのか?

- どのようなサプライチェーンやバリューチェーンの動向が市場に影響を与えているのか?

- 将来の市場成長に影響を及ぼす可能性のあるリスクや課題は何か?

- どのような顧客需要のパターンが業界のあり方を変えつつあるのか?

- サステナビリティへの取り組みは、将来の市場の発展にどのような影響を与えるのか?

- 市場参加者に対して、どのような戦略的提言がなされているのか?

- 投資家や意思決定者は、どのようなビジネスチャンスを優先すべきか?

業界のリーダーがSDKI Analyticsを選ぶ理由

日本に特化した情報

グローバルな視点から日本市場を深く理解します

堅牢な研究方法論

実績のあるフレームワークに裏付けられた一次調査および二次調査

品質およびデータ保証

正確な知見を保証する厳格な検証プロセス

専門アナリストによるサポート

ご購入前とご購入後の専用サポート

カスタムリサーチソリューション

お客様の特定のビジネスニーズに合わせた調査

エンタープライズライセンス

チームや組織向けの柔軟なライセンスオプション

グローバル展開(50以上の業界)

主要産業全体にわたる包括的な情報

クライアントの成功事例

世界中の企業やステークホルダーが、弊社のデータインテリジェンス及びコンサルティングサービスを通じてどのように恩恵を受け、戦略的優位性を獲得したか、実例をご覧ください。これらのお客様の声は、インパクトのある成果をもたらす高品質なデータを提供するという弊社のコミットメントを反映しています。

よくある質問

178億米ドルの市場規模は、2035年までに達すると予測されています。

予測期間中の年平均成長率(CAGR)は7%です。

ご質問がございましたら、ご希望の方法でお問い合わせください。弊社のチームができるだけ早くご返答いたします。

会社名: SDKI Analytics

日本事務所

15/F セルリアンタワー, 桜丘町26-1、150-8512, 東京、渋谷区、日本

米国オフィス

600 S Tyler St Suite 2100 #140, Amarillo, TX 79101