- 2020ー2024年

- 2025ー2037年

- 必要に応じて日本語レポートが入手可能

品質と信頼の証

足と足首のデバイス市場規模

足と足首のデバイス市場に関する当社の調査レポートによると、市場は予測期間中に約 8% の CAGR で成長し、2037 年までに約 140億米ドルの価値に達すると予想されています。さらに、2025年の足と足首のデバイス市場調査規模は緩やかなペースで成長すると予想されます。しかし、当社の調査アナリストによると、2024 年の 足と足首のデバイス市場の収益は 50億米ドルになると記録されています。

足と足首のデバイス市場分析

足および足首のデバイスの分野では、数百万人が罹患している筋骨格系疾患の驚くべき増加が世界規模での差し迫った懸念となっています。世界保健機関によると、世界中で 17 億人以上がこのような症状に苦しんでおり、足と足首の問題がそのかなりの部分を占めています。高齢化で有名な国である日本から見ると、この問題はますます深刻になっています。日本は人口の27%以上が65歳以上であり、世界で最も高齢化が進んでいる国の一つとなっています。これにより、足や足首の広範囲にわたる障害が引き起こされています。関節炎と足底筋膜炎。統計によると、過去 10 年間に報告された症例は前年比 12% 増加しています。これは、世界、特に日本で直面する特有の課題に対応する高度な足と足首のデバイスが緊急に必要であることを浮き彫りにしています。人口の高齢化が問題を強調する場合 的を絞ったソリューションの開発と導入は、これらの問題に取り組む何百万もの人々の生活の質を大幅に向上させることができます。

当社の足と足首のデバイス市場分析によると、主な成長要因の一部は次のとおりです:

- 路上事故の増加 – 事故の余波で、多くの人が無数の怪我を負い、悲劇的には死亡事故につながるケースもあります。交通事故では、骨折、脱臼、軟部組織の損傷など、足と足首の損傷が特に多く発生します。医療専門家は、そのような傷害に対処しリハビリテーションを行うために、装具、サポート、整形外科用インプラントなど、足や足首のさまざまな器具を使用しています。世界的な交通事故発生率の増加は、医療提供者が需要の高まりに応えようと努める中、これらの専用機器の必要性が高まっていることを浮き彫りにしており、事故後の医療と回復においてこれらのイノベーションが果たす重要な役割を強調しています。 WHO によると、交通事故により年間約 1.19 百万人が死亡しています。世界の自動車使用量の約60%を交通事故が占めているにもかかわらず、世界の交通死亡事故の92%は低・中所得国で発生しています。

- 製品商品化に対する需要の高まり – 足および足首のデバイスは、従来の代替品と比較して、手頃な価格の強化、有効性の向上、優れた患者の快適さ、ユーザーフレンドリーな特性など、無数の利点をもたらします。注目すべきことに、著名な業界関係者が、足や足首のさまざまな疾患や変形の治療に徐々に力を入れており、一般的な市場ギャップに対処しています。エンドユーザーからの関心の高まりは、優れた治療結果が期待できる先進的な製品と治療法へのアクセスのしやすさに起因すると考えられます。この進化する状況は、業界が足と足首のヘルスケアの分野で高まる需要と期待に応えようと努めているため、イノベーションへの取り組みを強調しています。

日本のローカルプレーヤーにとっての足と足首のデバイス市場の収益創出ポケットは何ですか?

日本の足および足首のデバイス市場は、独自の人口動態トレンドと堅調な医療環境の組み合わせによって促進され、地元のプレーヤーに有利な収益を生み出すポケットを提供しています。かなりの割合の高齢者を特徴とする日本の高齢化により、足や足首の装置を含む整形外科用ソリューションの需要が急増しています。

日本市場の活力は、足と足首の装備に関連する輸出入データによって強調されています。日本は世界の医療機器産業の主要なプレーヤーであり、フットケア製品や足首ケア製品など、さまざまな種類の医療機器を輸出入しています。最近のデータによると、医療機器の生産率は81%です。高齢化する人口の特別なニーズを満たすために、この国では先進的な整形外科用機器の輸入が大幅に増加しています。いくつかの日本のメーカーおよび企業グループは、足および足首用デバイスの開発と革新に積極的に貢献しています。これらの企業は、増大する市場の需要に戦略的に対応しています。たとえば、地元のメーカーと研究機関とのパートナーシップにより、次世代の義足、矯正器具、その他の足や足首のデバイスの開発が促進されています。この協力的なアプローチは、技術の進歩を促進するだけでなく、この分野での雇用と専門知識を創出することで地域経済をサポートします。

さらに、日本企業は、高齢化人口に蔓延する足と足首の特定の症状に対応するために、製品ポートフォリオを多様化しています。関節炎、足底筋膜炎、その他の筋骨格系疾患に対するカスタマイズされたソリューションへの関心が高まっています。この戦略的転換は、日本国民の特別な医療ニーズを満たすだけでなく、世界の足と足首のデバイス市場に貢献する強力な立場に地元企業を置くことも目的としています。

市場課題

整形外科用機器市場は、製品の品質基準を管理する不確実な政府規制に起因する課題に直面しています。整形外科用インプラントやデバイスの使用には、挿入時の不快感や手術部位の感染の可能性などのリスクが伴います。足や足首の器具は、ニッケル、コバルト、クロム、チタンなどの金属で構成されることが多く、アレルギー、感染症、湿疹性皮膚炎、蕁麻疹、血管炎、骨溶解、痛み、無菌的緩みなどの合併症を引き起こす可能性があり、その普及が制限されています。

サンプル納品物ショーケース

- 調査競合他社と業界リーダー

- 過去のデータに基づく予測

- 会社の収益シェアモデル

- 地域市場分析

- 市場傾向分析

足と足首のデバイス市場レポートの洞察

|

足と足首のデバイス市場規模とシェアレポートの洞察 |

|

|

CAGR |

8% |

|

予測年 |

2025-2037年 |

|

基準年 |

2024年 |

|

予測年の市場価値 |

約140億米ドル |

足と足首のデバイス市場セグメンテーション

当社は、足と足首のデバイス市場に関連するさまざまなセグメントにおける需要と機会を説明する調査を実施しました。製品タイプ、 アプリケーション、エンドユーザーごとに市場を分割しました。

足と足首のデバイス市場は、製品タイプ別に基づいて、整形外科用インプラントおよび装置、固定装置および支持装置、プロテーゼにさらに分類されています。 整形外科用インプラントおよび整形外科用デバイスは、2037 年までに 43% の最大の市場シェアを保持すると予想されています。糖尿病は筋骨格系の合併症を伴うことが多く、整形外科的介入の必要性が高まっているため、糖尿病の発症率の増加が整形外科用デバイス市場の重要な推進要因となっています。 国際糖尿病連盟によると、成人 537百万人(20―79 歳)が 10 人に 1 人の割合で糖尿病を抱えています。この数は 2030 年までに 643百万人、2045 年までに 783百万人に達すると予想されています。同時に市場は、テクノロジーとデザインの進歩を示す継続的な新製品の発売です。これらのイノベーションは、進化する医療ニーズに応えるだけでなく、消費者の関心を刺激し、競争的な市場環境を促進します。さらに、ブランドの整形外科用機器やインプラントの採用が増えていることは、主に有名ブランドに関連する優れた品質と信頼性が認知されていることによって、確立されたメーカーに対する認識と信頼が高まっている証拠です。この需要の急増は、患者と医療提供者が整形外科用ソリューションの有効性と耐久性を優先するという広範な傾向を示しており、整形外科用機器市場の成長軌道をさらに推進しています。

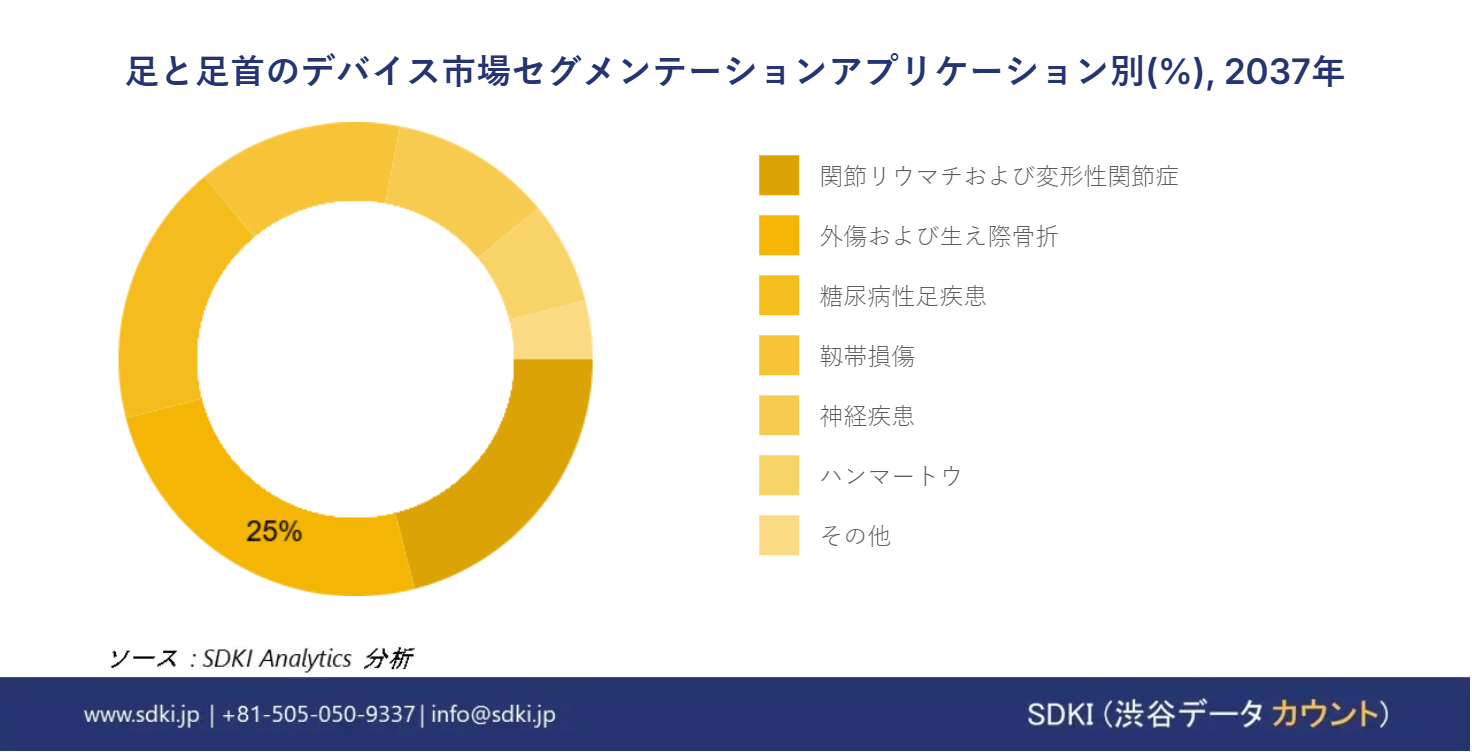

さらに、足と足首のデバイス市場は、アプリケーションに基づいて、外傷および生え際骨折、関節リウマチおよび変形性関節症、糖尿病性足疾患、靱帯損傷、神経疾患、ハンマートウ、その他に細分化されています。 外傷および髪の生え際の骨折は、2037 年までに 25% の最大の市場シェアを占めると予想されています。スポーツ傷害や交通事故の蔓延は増加傾向にあり、高度な整形外科的介入が必要となっています。特に骨折に関連した足と足首の再建手術の件数が増加していることも、このカテゴリーにおける需要の急増にさらに寄与しています。足と足首の靱帯損傷は、特にスポーツにおいて大人と子供の両方に蔓延しており、専門的な整形外科的解決策が不可欠であることが強調されています。足や足首の重傷が長期的な障害や病気につながる可能性を考えると、外傷に焦点を当てたデバイスの重要性が最も重要になります。この分野の軌道は、世界的な人口高齢化と洗練された足と足首の製品の継続的な進歩によっても推進されており、今後数年間の持続的な成長を示しています。

|

製品タイプ |

|

|

アプリケーション |

|

|

エンドユーザー |

|

足と足首のデバイス市場の動向分析と将来予測:地域概要

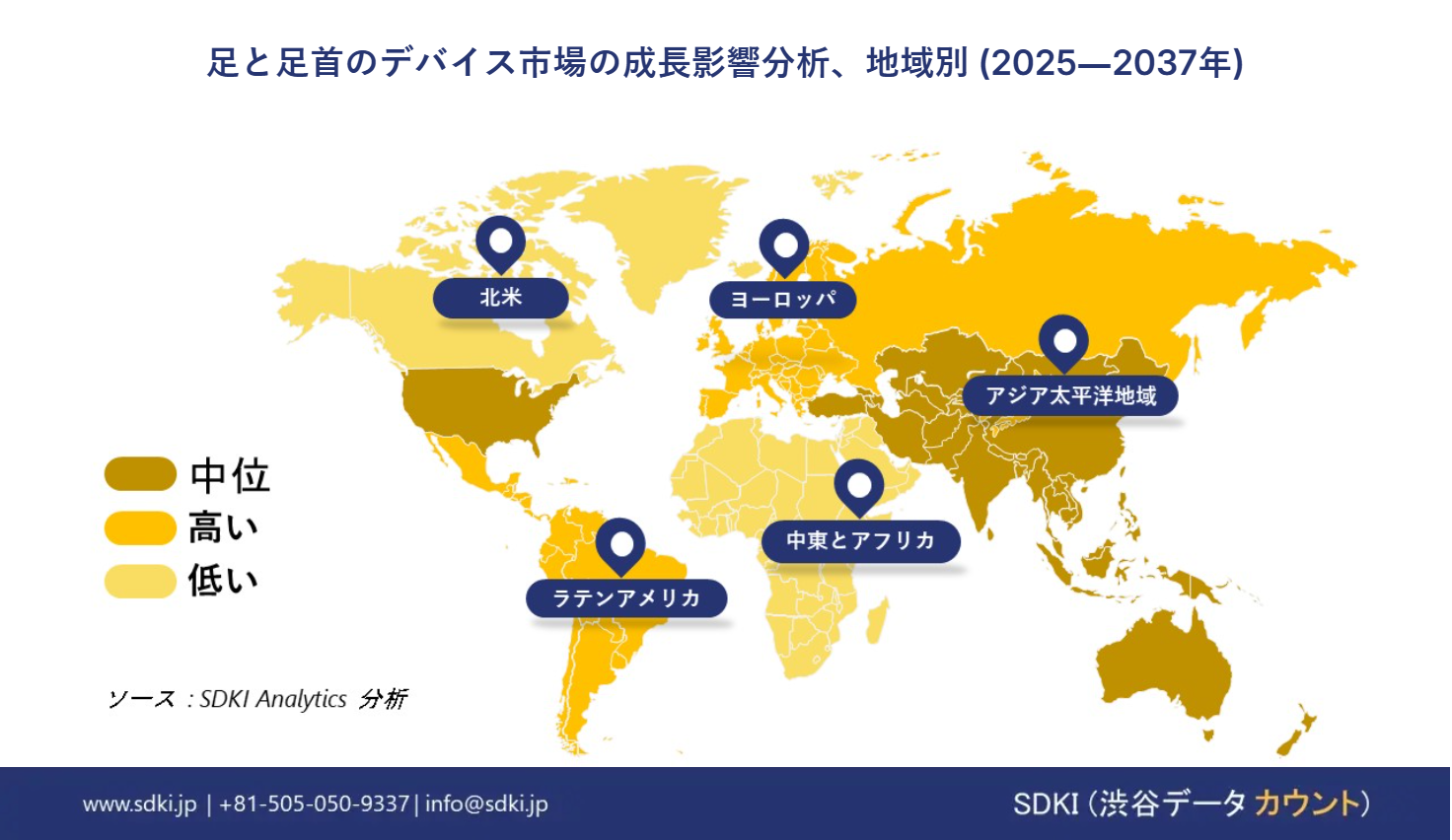

アジア太平洋地域は、予測期間中に市場で 27% の最も速い成長を記録すると予想されます。インド、中国、日本などの主要国で急成長している医療インフラは、この地域の足首および足のデバイスの需要を促進する上で極めて重要な役割を果たしています。医療ツーリズム産業の堅調な拡大により、この需要はさらに拡大しています。足と足首のインプラントの増加は、診断ツールの改善と慢性整形外科疾患の発生率の増加の直接の結果です。中国において、足および足首のデバイスの成長要因となると、主な要因は足および足首の疾患の有病率の増加です。これは、人口の高齢化、ライフスタイルの変化、スポーツ関連の怪我の増加などの要因によるものです。中国の医療改革と可処分所得の増加が市場をさらに牽引しています。同様に、韓国でも成長の原動力は中国と似ています。高齢者人口の増加とライフスタイルの変化と相まって、足と足首の疾患の有病率の増加が、これらのデバイスの需要に貢献しています。

日本では、医療技術の進歩と足と足首の健康に対する意識の高まりがこの市場の成長に貢献しています。日本の国民の健康意識が高まるにつれ、予防策や整形外科の問題に対処するための革新的なソリューションへの関心が高まっています。

|

北米 |

|

|

ヨーロッパ |

|

|

アジア太平洋地域 |

|

|

ラテンアメリカ |

|

|

中東とアフリカ |

|

北米は、2037 年までに世界市場の 32% という主要なシェアを占めると予想されています。北米市場の力強い成長はさまざまな要因によって推進されており、高い受け入れ率と患者にとっての手頃な価格が極めて重要な役割を果たしています。スポーツ傷害の発生率の増加により、足および足首の先進的なデバイスの需要がさらに高まっています。また、この地域では技術進歩を積極的に取り入れているため、ヘルスケア分野のイノベーションが促進され、足と足首のデバイス市場にプラスの影響を与えています。高齢者はしばしば整形外科的介入を必要とするため、高齢化人口の拡大により市場の勢いが増しています。

足と足首のデバイス調査の場所

北米(米国およびカナダ)、ラテンアメリカ(ブラジル、メキシコ、アルゼンチン、その他のラテンアメリカ)、ヨーロッパ(英国、ドイツ、フランス、イタリア、スペイン、ハンガリー、ベルギー、オランダおよびルクセンブルグ、NORDIC(フィンランド、スウェーデン、ノルウェー) 、デンマーク)、アイルランド、スイス、オーストリア、ポーランド、トルコ、ロシア、その他のヨーロッパ)、ポーランド、トルコ、ロシア、その他のヨーロッパ)、アジア太平洋(中国、インド、日本、韓国、シンガポール、インドネシア、マレーシア) 、オーストラリア、ニュージーランド、その他のアジア太平洋地域)、中東およびアフリカ(イスラエル、GCC(サウジアラビア、UAE、バーレーン、クウェート、カタール、オマーン)、北アフリカ、南アフリカ、その他の中東およびアフリカ

競争力ランドスケープ

足と足首のデバイス業界の概要と競争のランドスケープ

SDKI Inc. の調査者によると、足と足首のデバイス市場は、大企業と中小規模の組織といったさまざまな規模の企業間の市場競争により細分化されています。市場関係者は、製品や技術の発売、戦略的パートナーシップ、コラボレーション、買収、拡張など、あらゆる機会を利用して市場での競争優位性を獲得しています。

世界の足と足首のデバイス市場の成長に重要な役割を果たす主要な主要企業には、Stryker、Zimmer Biomet.、Smith & Nephew plc、Arthrex, Inc.、Integra LifeSciencesなどが含まれます。 さらに、日本の足と足首のデバイス市場のトップ5プレーヤーは、GUNZE LIMITED.、Japan Medical Dynamic Marketing, Inc.、Acumed LLC.、 NIPPON SIGMAX Co., Ltd.、 およびObara Kogyo, Inc.などです。 この調査には、世界の足と足首のデバイス市場分析レポートにおける詳細な競合分析、企業概要、最近の動向、およびこれらの主要企業の主要な市場戦略が含まれています。

足と足首のデバイス市場ニュース

- 2023 年 12 月、Henry Schein, Inc. は、当社の長年の戦略に沿って、整形外科市場の上肢および下肢の専門分野に参入する計画を発表しました。

- 2023年1月、Gunzeは、糖尿病性足部潰瘍や慢性静脈不全による難治性潰瘍の治療を目的とした日本初のヒト羊膜製品「エピフィックス」の販売開始を発表しました。

足と足首のデバイス主な主要プレーヤー

主要な市場プレーヤーの分析

日本市場のトップ 5 プレーヤー

目次

足と足首のデバイスマーケットレポート

関連レポート

よくある質問

- 2020ー2024年

- 2025ー2037年

- 必要に応じて日本語レポートが入手可能

品質と信頼の証